The official settlement balance

The official settlements balance focuses on the operations that the monetary authorities have to undertake to finance any imbalance in the current and capital accounts.With the settlements concept, the autonomous items are all the current and capital account transactions including the statistical error, while the accommodating items are those transactions that the monetary authorities have undertaken as indicated by the balance of official financing.The current account and capital account items are all regarded as being induced by independent households, firms, central and local government and are regarded as the autonomous items.If the sum of the current and capital accounts is negative, the country can be regarded as being in deficit as this has to be financed by the authorities drawing on their reserves of foreign currency, borrowing from foreign monetary authorities or the International Monetary Fund.

A major point to note with the settlements concept is that countries whose currency is used as a reserve asset can have a combined current and capital account deficit and yet maintain fixed parity for their currency without running down their reserves or borrowing from the IMF.This can be the case if foreign authorities eliminate the excess supply of the domestic currency by purchasing it and adding it to their reserves.This is particularly important for the United States since the US dollar is the major reserve currency.The United States can have a current account and capital account deficit which is financed by increased foreign authorities’ purchases of dollars and dollar treasury bills—in other words, increased US liabilities constituting foreign authorities’ reserves.For this reason, part of the official settlements balance records changes in liabilities constituting foreign authorities’ reserves.

The official settlements concept of a surplus or deficit is not as relevant to countries that have floating exchange rates as it is to those with fixed exchange rates.This is because if exchange rates are left to float freely the official settlements balance will tend to zero because the central authorities neither purchase nor sell their currency, and so there will be no changes in their reserves.If the sales of a currency exceed the purchases then the currency will depreciate, and if sales are less than purchases the currency appreciates.The settlements concept is, however, very important under fixed exchange rates because it shows the amount of pressure on the authorities to devalue or revalue the currency.Under a fixed exchange-rate system a country that is running an official settlements deficit will find that sales of its currency exceed purchases, and to avert a devaluation of the currency authorities have to sell reserves of foreign currency to purchase the home currency.On the other hand, under floating exchange rates and no intervention the official settlements balance automatically tends to zero as the authorities do not buy or sell the home currency since it is left to appreciate or depreciate.

Even in a fixed exchange-rate regime the settlements concept ignores the fact that the authorities have other instruments available with which to defend the exchange rate, such as capital controls and interest rates.Also, it does not reveal the real threat to the domestic currency and official reserves represented by the liquid liabilities held by foreign residents who might switch suddenly out of the currency.

Although in 1973 the major industrialized countries switched from a fixed to a floating exchange-rate system, many developing countries continue to peg their exchange rate to the US dollar and consequently attach much significance to the settlements balance.Indeed, to the extent that industrialized countries continue to intervene in the foreign exchange market to influence the value of their currencies, the settlements balance retains some significance and news about changes in the reserves of the authorities is of interest to foreign exchange dealers as a guide to the amount of official intervention in the foreign exchange market.

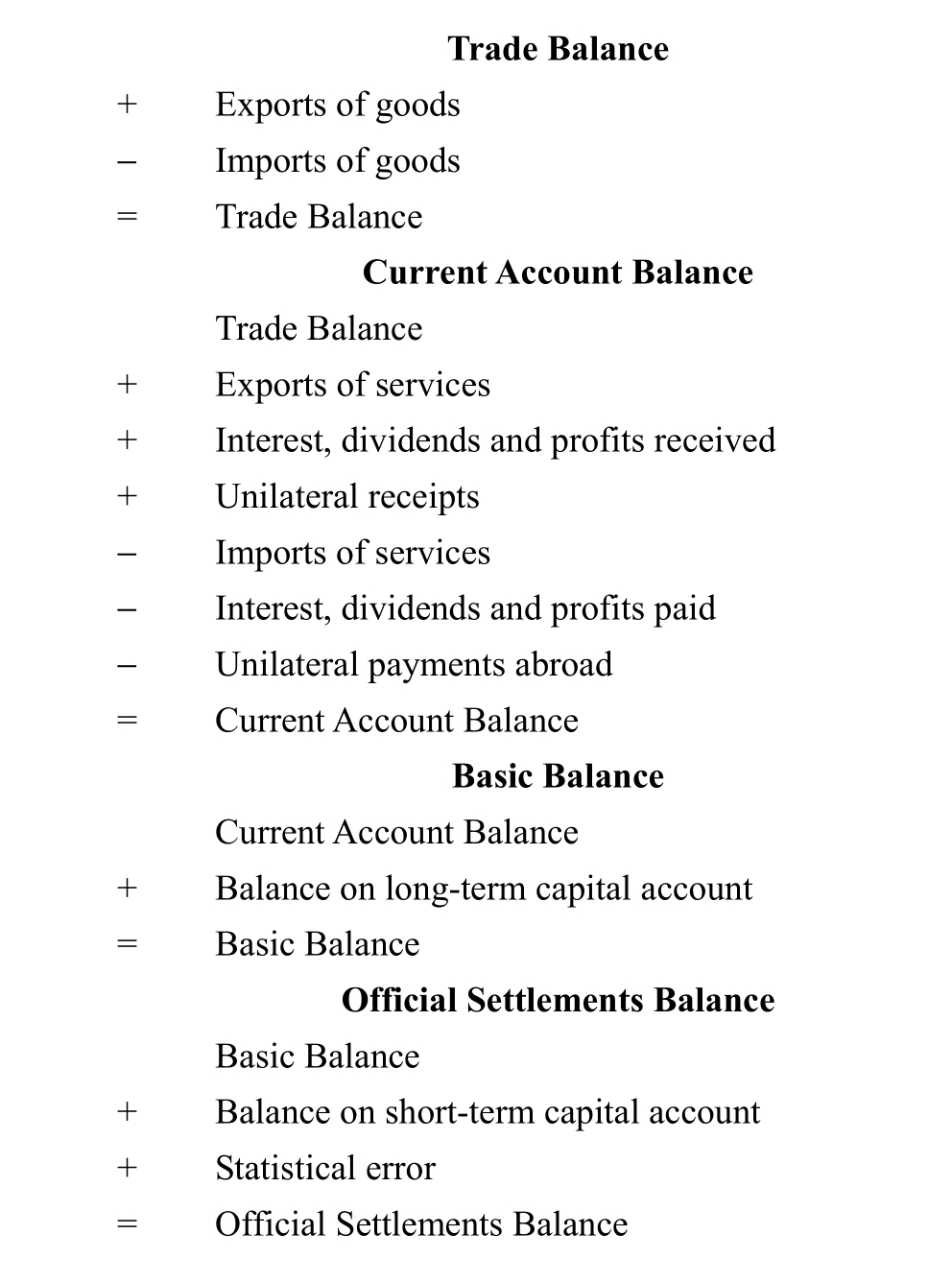

The IMF provides an annual summary of the balance-of-payments statistics using these alternative concepts of balance-of-payments disequilibrium.A summary of key concepts is shown in Table 1.2.

Table 1.2 Summary of key balance-of-payments concepts