Chapter 7 Currency Futures, Options and Swaps

Exercises

1.Single-choice questions

cabbc

cbaaa

bdcab

accbbc

2.True/False questions

TFTFF

TTFFF

TTTTT

3.Essay questions

(1)

It is an important type of swap on international financial markets.This is a contract under which one party commits itself to exchange a set of interest payments that it is scheduled to receive for different set of interest payments owed to another party.

(2)

Enter into a forward contract to buy 40 million euros in 90 days.

The forward rate is $1.11/euro, therefore the company must deliver $44.4 million in 90 days.This way the company has an asset position in euro through the forward contract that covers its liability of the 40 million euro loan.

(3)

a.If the £ rose to $1.92 in 6 months, the US company would exercise the pound call option.The sum of the strike price and premium is

$1.90+ $0.023 = $1.9230/£

This is bigger than $1.92.

So hedging in the options market is not better.

b.When we say the company can break even, we mean that hedging or not hedging doesn’t matter.And only when (strike price + premium)= the exchange rate, hedging or not doesn’t matter.So, the exchange rate =$1.923/£.

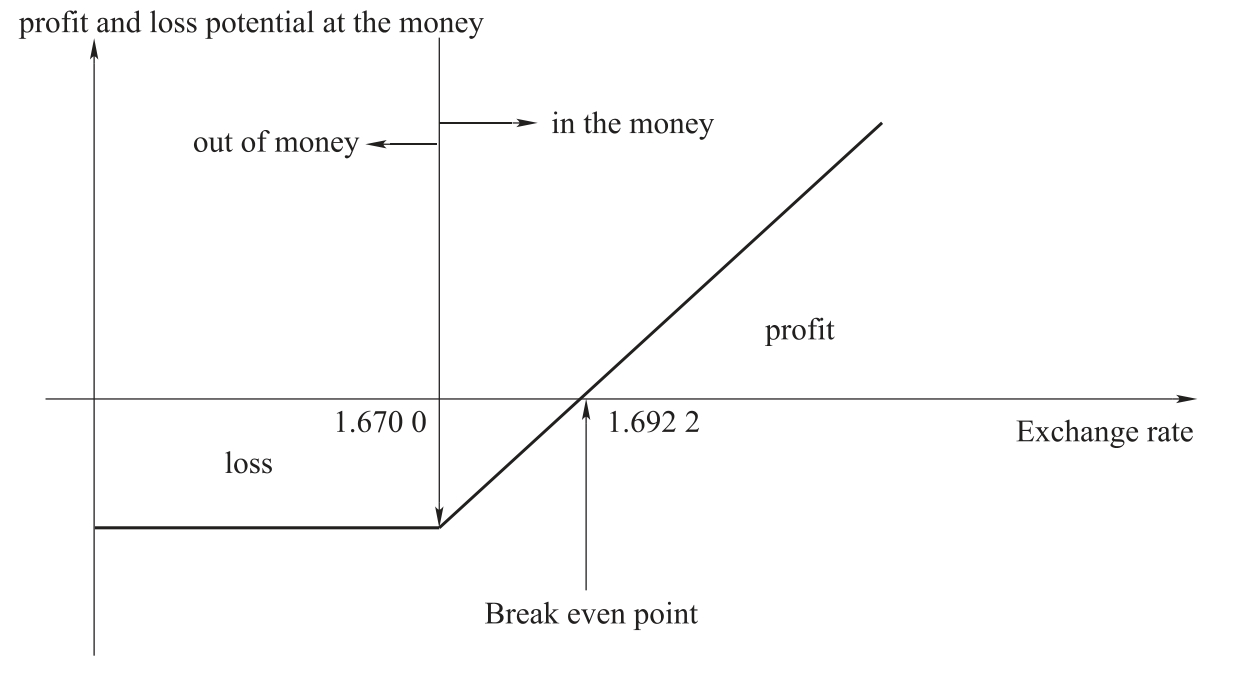

(4)

Following diagram shows the profit and loss potential, and the break-even price of this put option:

(5)

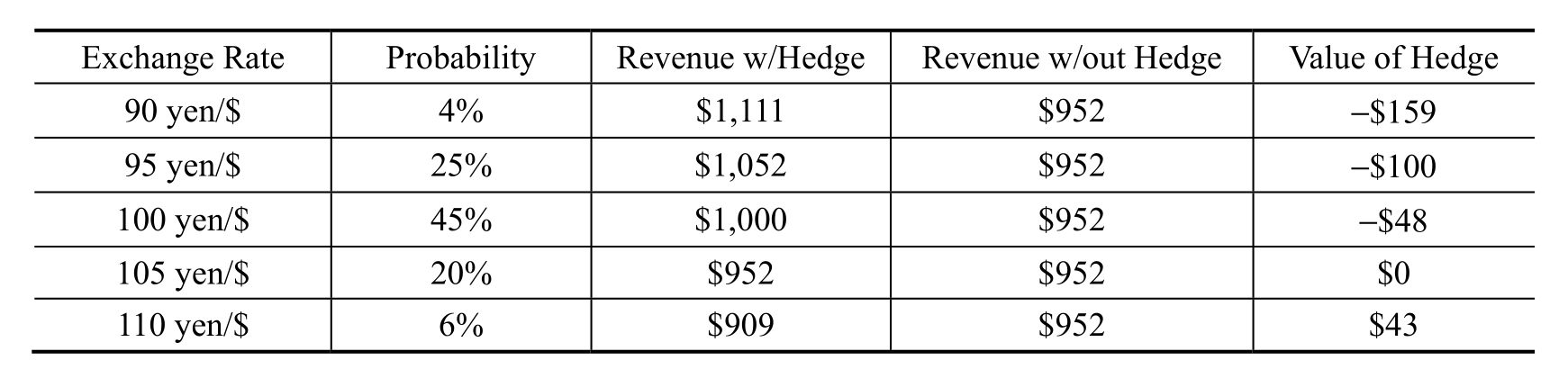

a.You are expecting revenues of 100,000 yen in one month that you will need to covert to dollars.You could hedge this in forward markets by taking long positions in US dollars (short positions in Japanese yen).By locking in your price at $1 = 105 yen, your dollar revenues are guaranteed to be

100,000 yen/ 105 = $952

On the other hand, you can wait and use the spot markets.

b.Expected Value = (0.02)(-159)+ (0.25)( -100)+ (0.45)( -48)+ (0.20)(0)+ (0.08)(43)

= -$24

c.You could replicate this hedge by using the following:

(a)Borrow in Japan

(b)Convert the yen to dollars

(c)Invest the dollars in the US

(d)Pay back the loan when you receive the 100,000 yen

(6)

a.Currency futures contracts entail daily cash follow settlements, whereas currency forward contracts entail a single settlement only at the date of maturity.

b.Futures contracts typically involve smaller currency denominations as compared with forward contracts.

c.Large banking institutions and corporations that transmit large volumes of foreign currencies are the primary users of forward contracts.Individuals and smaller firms that wish to undertake hedging or speculative strategies typically trade currency futures.

d.Currency futures contracts have higher liquidity and can be transferred freely while currency forward contracts cannot.

e.Buyers and sellers of Currency futures contracts need to pay Future guarantee by a certain ratio.