Money expansion through the Eurocurrency markets

The best way to illustrate how the Eurocurrency market functions is with an example.We can start with a commercial transaction.

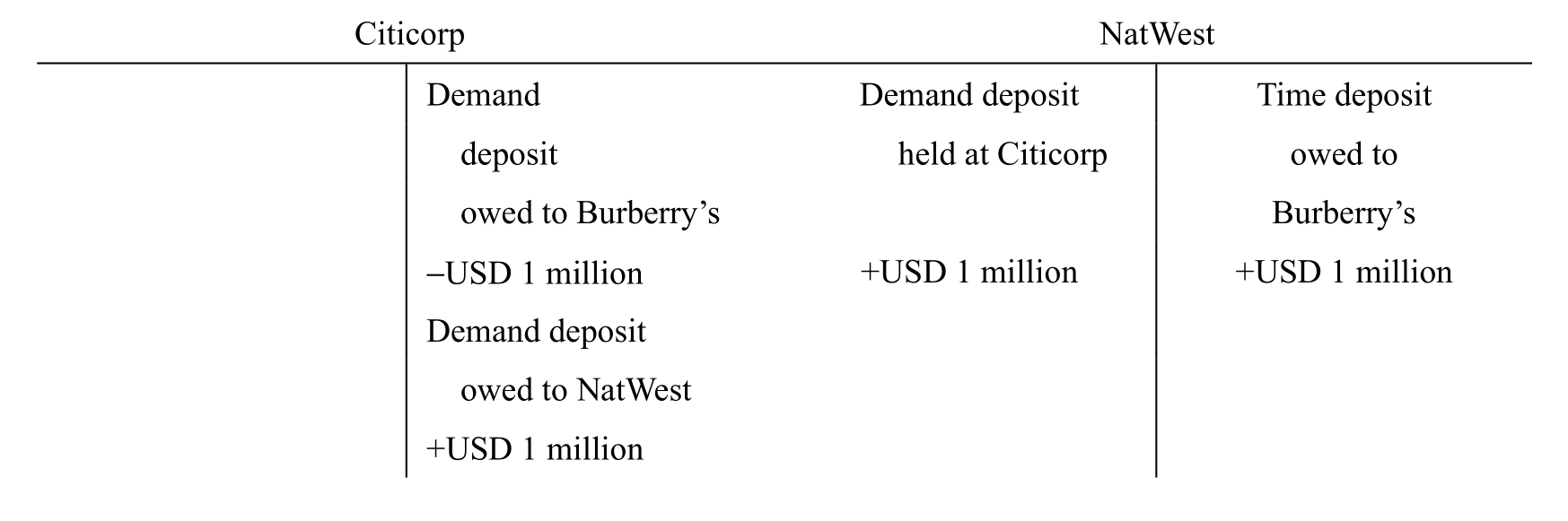

Transaction 1

Suppose that Burberry’s, a British clothes-maker, sells US Corporation, an American importer, USD 1 million worth of merchandise.The goods are billed in dollars and US Corporation pays with a check drawn on its New York bank.Burberry’s has an account at Citicorp in New York and deposits the check there.Citicorp’s external position (its position vis-a-vis non-residents)as a result of this transaction will be as follows:

Transaction 2

Burberry’s needs dollars for working capital purposes but wants to earn interest and decides to put the USD 1 million into a seven-day time deposit.Its London bank, NatWest, is paying higher rates than Citicorp so Burberry’s instructs Citicorp to transfer the USD 1 million to NatWest in London.This transaction will be recorded by the two banks as follows:

The USD 1 million time deposit owed to Burberry’s is a Eurodollar deposit that NatWest has created by borrowing from Burberry’s.Although the time deposit is in US dollars, NatWest is outside the jurisdiction of the US authorities and the conditions of the loan are not subject to any US regulations on bank deposits, interest rates and the like.Notice that Citicorp’s total external position is unchanged.It still has a total of USD 1 million in demand liabilities vis-a-vis non-residents.The only thing that has changed for Citicorp is that the demand liability is owed to NatWest instead of to Burberry’s.

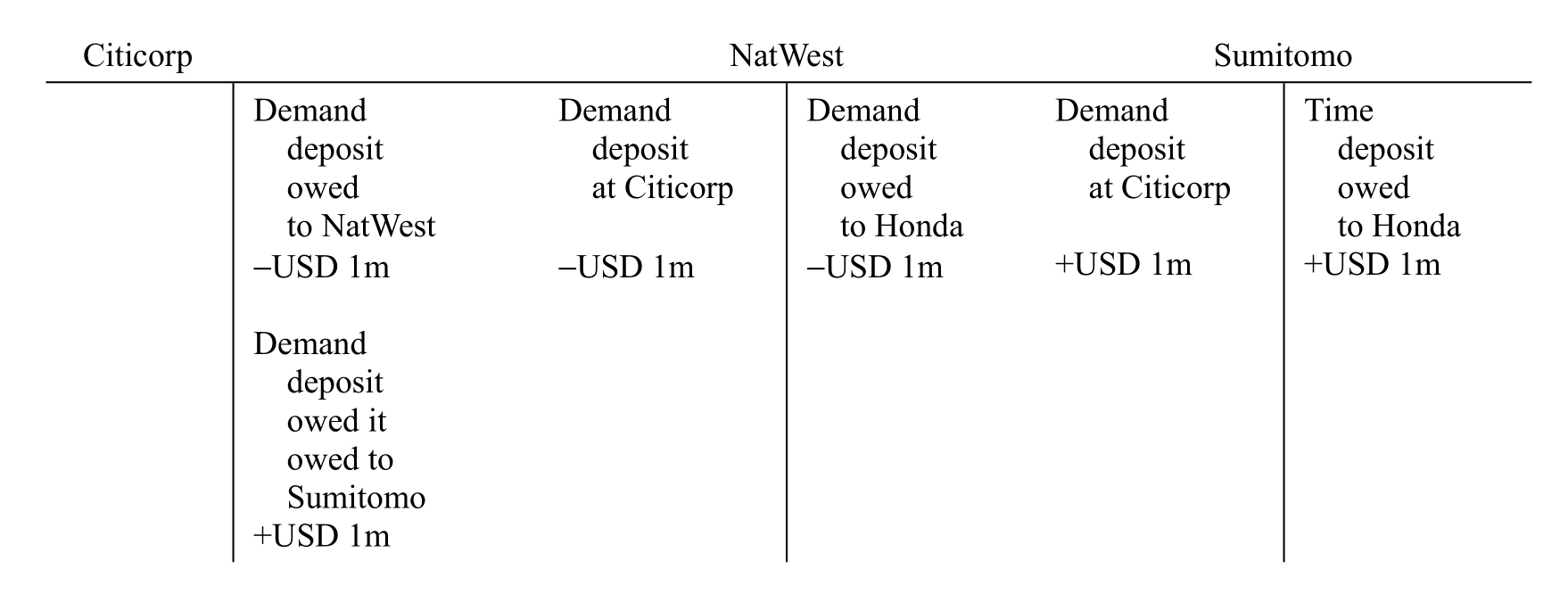

Transaction 3

The funds that NatWest is holding with Citicorp in New York are earning lower interest than the interest it is paying to Burberry’s on the time deposit.This is very costly, so if there were no commercial borrowers available, NatWest would deposit the funds in the interbank market.Fortunately, Honda, a Japanese automaker, has approached NatWest about a six-month, USD 1 million loan.Because Honda is a high-quality customer, NatWest agrees to the loan at Libor plus![]() %.

%.

When the loan is extended the funds are initially made available to Honda in the form of demand deposit at NatWest.The transactions for the two banks will be recorded as follows:

Notice that Citicorp is not affected by the transaction because there is no transfer of funds.However, NatWest has effectively created USD 1 million in the form of a demand deposit owed to Honda.This is the type of operation that those who feared unlimited money supply multiplication were referring to.There are now USD 2 million of liabilities owed by non-US banks backed by only USD 1 million of claims on US banks.

Transaction 4

Honda wants the proceeds of the loan transferred to the Sumitomo Bank in Japan where the money will earn interest in a time deposit until used.NatWest sends a telex to Citicorp in New York, instructing it to transfer USD 1 million to Honda’s account with Sumitomo in Japan.This transaction will be recorded with the three banks as follows:

There are still USD 2 million of Eurodollars, only now Sumitomo has acquired dollar balances.Citicorp’s external position is still USD 1 million of demand liabilities, owed now to Sumitomo.

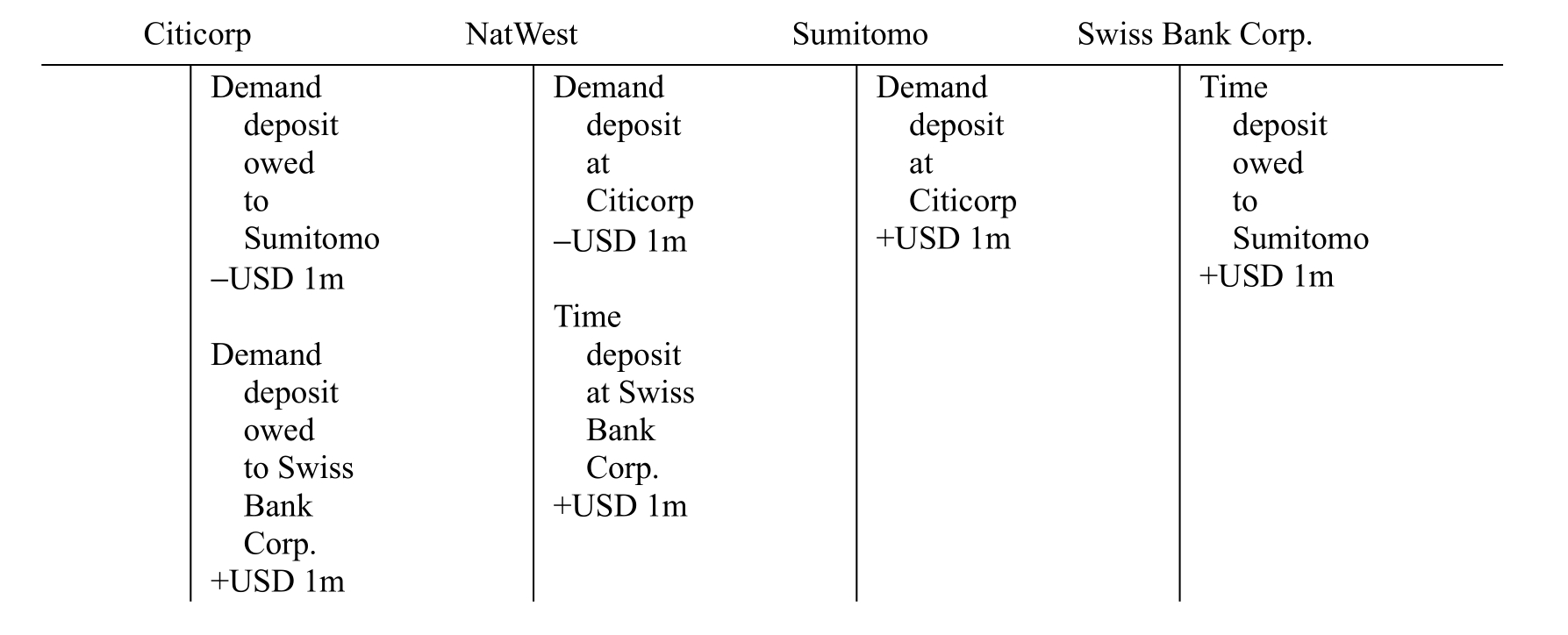

Transaction 5

Sumitomo is in the same position that NatWest was in when it took the time deposit from Burberry’s.It is paying higher interest on the time deposit than its demand deposit held with Citicorp is earning.Sumitomo has no loan prospects in sight so it decides to place the money in the interbank market.After casting around for quotes, it finds that Swiss Bank Corp.in Switzerland is offering the best rate.Sumitomo instructs Citicorp to credit its account with Swiss Bank Corp.The transactions for the four banks will be recorded as follows:

A new Eurodollar deposit has been created in the form of a time deposit that Sumitomo is holding with Swiss Bank Corp.There are now USD 3 million worth of Eurodollars in the system.Citicorp’s external position is still the same: only the owner of the deposit has changed.If Swiss Bank Corp.decides to leave its dollars with Citicorp, no more Eurodollars will be created.The same is true if Swiss Bank Corp.decides to transfer its dollar claim to another US bank.When dollars are redposited in the United States the multiplicative process comes to an end.This is the first way that funds can “leak” out of the Eurocurrency system and bring the multiplicative process to an end.

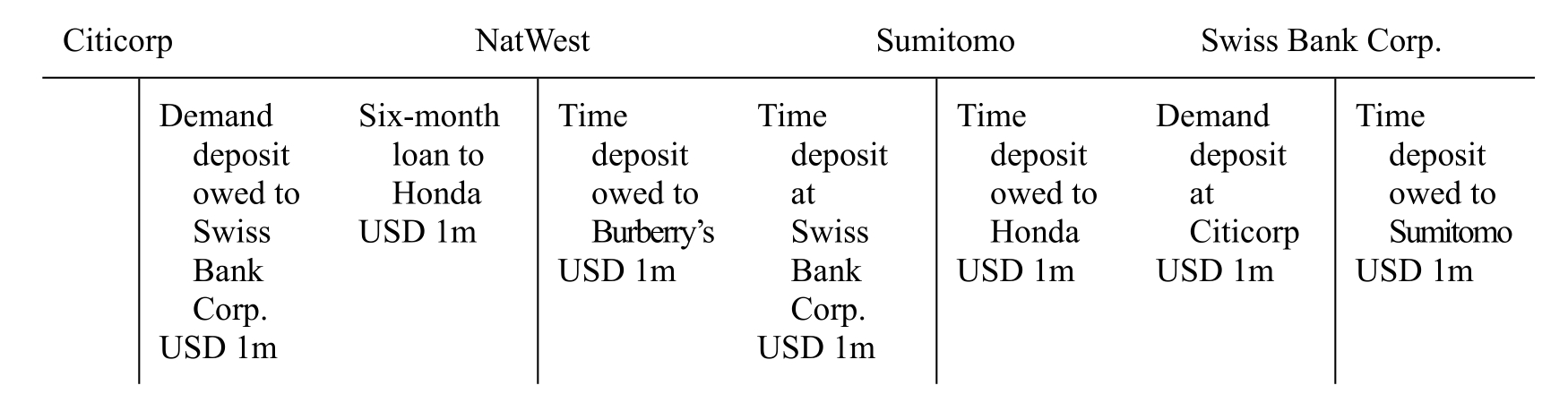

We can consolidate the foregoing transactions and see how the balance sheet of each bank will look at the end of Transaction 5:

Citicorp has USD 1 million in external liabilities and there are USD 3 million in Eurodollar liabilities.This balance sheet is the result of the three basic operations involved in the Eurocurrency market.After the commercial transaction (Burberry’s export to the United States)they were successively:

1.A private loan to the banking system (Burberry’s time deposit with NatWest).

2.A commercial loan to the non-bank sector (NatWest’s six-month loan to Honda).

3.An interbank Joan (Sumitomo’s loan to Swiss Bank Corp.).

Most of these transactions involve a bank in the currency’s domestic market.In our case Citicorp was involved in most of the transactions.For a short period of time it was not involved in the Honda transaction and if Honda had decided to hold its deposit with NatWest, it would not have become involved.However, this situation can only be shortlived.Borrowers borrow to make payments.When payments are made and recipients do not bank at NatWest, Citicorp will be involved in the transfer of funds to the different banks receiving payments.

It seems that Eurodollar expansion is limitless, stopping only when some bank decides to hold its funds in the United States.In fact, reality is far more reassuring.In the first place, if a Eurobank makes a Eurodollar loan and the proceeds are transferred or spent in the United States, the multiplication will also be ended.This is the second way that dollars can “leak” from the Eurocurrency system.For example, in Transaction 4, if Honda had transferred its funds to Citicorp instead of to Sumitomo, Citicorp’s external liability would have disappeared from the Eurobanking system and no more Eurodollars would have been created.Furthermore, Eurodollar creation does not depend just on the ability of Eurobanks to offer slightly better rates than US banks.Dollars must compete with other currencies for borrowing and lending purposes.If borrowers and lenders find that they are better off borrowing and lending in another currency, they will sell dollars for the other currency, thereby reversing the multiplicative process.

Transaction 6

Suppose, for example, that when Honda’s time deposit matures, the company decides that sterling is a better investment than dollars.Honda thus sells dollars for pounds at the rate of USD 2 = GBP 1 and leaves its sterling in a demand deposit with Sumitomo.This transaction will be recorded by Sumitomo as follows:

The first thing to notice is that the outstanding amount of Eurodollars has been reduced by USD 1 million.A sale of dollars for another currency is thus the third way that dollars can “leak” from the system and reverse the multiplicative process.The second thing to notice is that Sumitomo now has a liability in sterling and an asset in dollars.Such an unbalanced position leaves Sumitomo exposed to a loss if the value of the dollar falls with respect to the pound.In practice Euro banks try to stay well hedged, which means that they generally try to balance their assets and liabilities in terms of currencies.Consequently, Sumitomo is likely to try to balance its position by selling dollars for pounds, which will reduce the outstanding amount of Eurodollars by USD 1 million more.

Thus, redepositing or spending Eurodollars in the United States stops the multiplicative process and sales of Eurodollars reverses it.Estimates of the actual multiplicative power of the Eurocurrency markets varies.Klopstock argues that leakage from the system is such that the multiplier is barely larger than 1.Clendenning and Meyer find that leakage is seriously reduced insofar as central banks redeposit their reserves in the Eurocurrency markets.Following this reasoning, Hewson and Sakakibara, estimate the multiplier at between 3 and 7.

Swoboda estimates its value at about 2.We ourselves find that the multiplier is 3.091with a one-year lag.