Eurocurrency interest rates

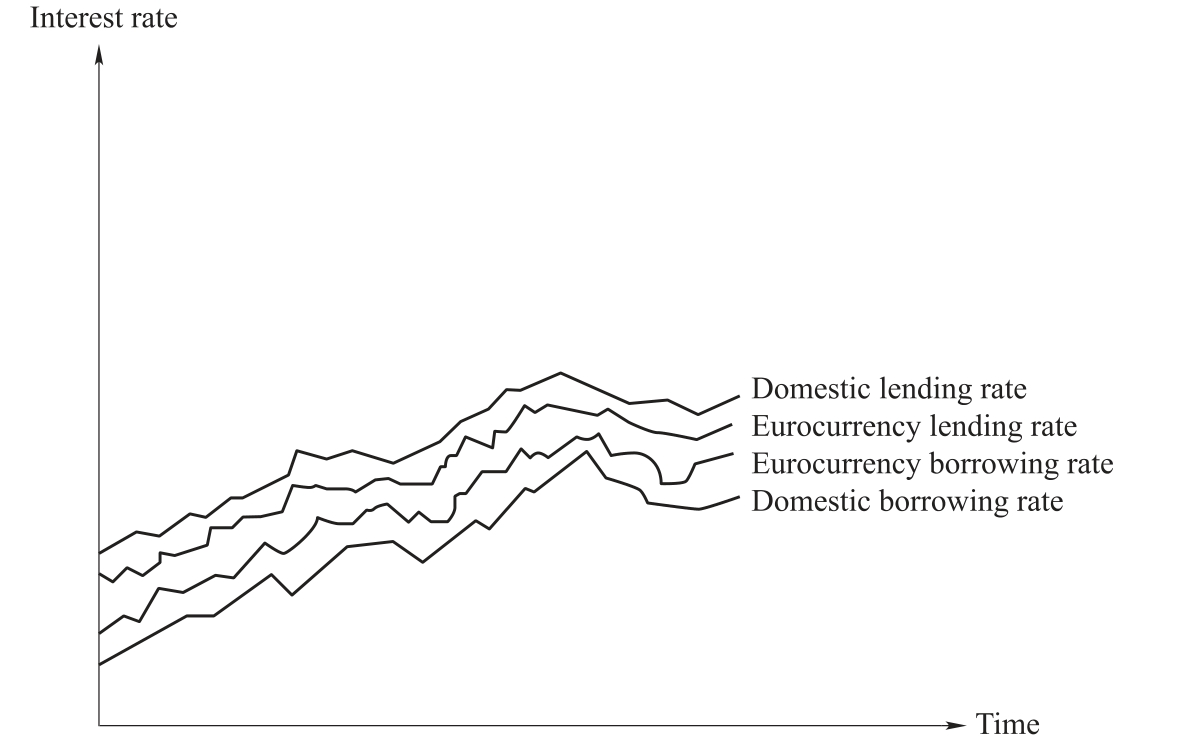

As we have suggested, Eurocurrency rates are closely related to the rates in the currency’s home market but, because of lower costs, spreads are lower.Spreads refer to the difference between borrowing rates and lending rates.Tighter spreads mean that the Eurocurrency markets offer slightly higher interest rates to lenders and slightly lower rates to borrowers than are available in the home market.Figure 10.1 shows how the smaller spread in the Eurocurrency market makes it possible for banks to offer better borrowing and lending rates than the domestic market.Notice that the trend of the Eurocurrency rates follows the trend of domestic interest rates without being perfectly parallel.Because of arbitrage, interest rates in the domestic and Eurocurrency markets can only differ insofar as there are additional costs, controls or risks involved in moving funds between one market and the other.Otherwise, arbitragers would borrow in the market where funds were cheaper and lend them where they are dearer, thereby causing the difference to disappear.

Because the cost of shifting funds from one market to another is negligible, substantial interest rate differentials between the domestic market and the Euromarket suggest the presence of differences in perceived risk or effective controls.For many years Eurofranc rates were considerably higher than domestic rates due to French restrictions on loaning abroad combined with domestic credit controls.With the supply limited, credit-starved French borrowers dodging the domestic controls maintained the differential by borrowing Eurofrancs whenever the interest rate began to fall.On the other side of the coin, Euro and euro Swiss franc rates have seen periods when they were considerably lower than domestic rates because of measures seeking to discourage capital inflows.One such measure was minimum reserves on certain types of nonresident deposits, which raised the cost of funds for domestic banks borrowing abroad.This caused them to lower the rate they were willing to pay for foreign funds to bring their total cost into line with the cost of domestic funds.In both cases controls caused considerable interest rate differentials between the two markets.Controls designed to restrict capital outflows will tend to push the Eurocurrency rate above the domestic rate while controls designed to restrict capital inflows will tend to push the Eurocurrency rate below the domestic rate.

Anticipating controls that do not yet exist can also cause an interest rate differential.If there is a possibility that at some future date funds will be unable to cross the border, investors will require a premium for holding assets in the domestic market.In this case the interest rate differential is due to higher perceived risk on assets held in the domestic market.

Figure 10.1 Domestic and Eurocurrency borrowing and lending rate spreads