Eurocurrency interest rates: LIBOR

In the Eurocurrency market, the reference rate of interest is the London Interbank Offered Rate (LIBOR).LIBOR is now the most widely accepted rate of interest used in standardized quotations, loan agreements, and financial derivatives valuations.LIBOR is officially defined by the British Bankers Association (BBA).For example, US dollar LIBOR is the mean of 16 multinational banks’ interbank offered rates as sampled by the BBA at 11 a.m.London time in London.Similarly, the BBA calculates the Japanese yen LIBOR, euro LIBOR, and other currency LIBOR rates at the same time in London from samples of banks.

The interbank interest rate is not, however, confined to London.Most major domestic financial centers construct their own interbank offered rates for local loan agreements.These rates include PIBOR (Paris Interbank Offered Rate), MIBOR (Madrid Interbank Offered Rate), SIBOR (Singapore Interbank Offered Rate); and FIBOR (Frankfurt Interbank Offered Rate), to name but a few.

The key factor attracting both depositors and borrowers to the Eurocurrency loan market is the narrow interest rate spread within that market.The difference between deposit and loan rates is often less than l%.Interest spreads in the Eurocurrency market are small for a number of reasons.Low lending rates exist because the Eurocurrency market is a wholesale market, where deposits and loans are made in amounts of $500,000 or more on an unsecured basis.Borrowers are usually large corporations or government entities that qualify for low rates because of their credit standing and because the transaction size is large.In addition, overhead assigned to the Eurocurrency operation by participating banks is small.

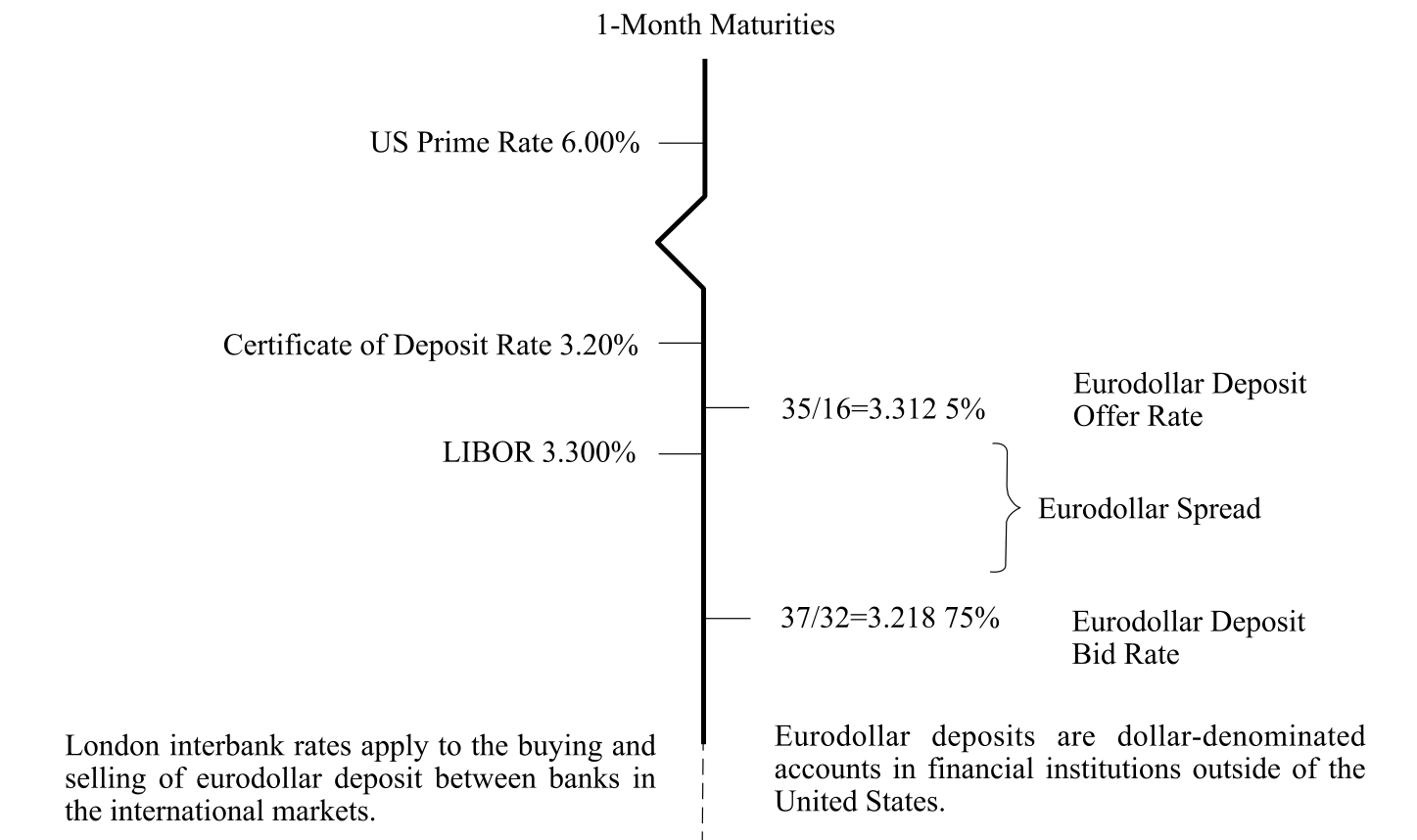

Deposit rates are higher in the Eurocurrency markets than in most domestic currency markets because the financial institutions offering Eurocurrency activities are not subject to many of the regulations and reserve requirements imposed on traditional domestic banks and banking activities.With these costs removed, rates are subject to more competitive pressures, deposit rates are higher, and loan rates are lower.A second major area of cost avoided in the Eurocurrency markets is the payment of deposit insurance fees (such as the Federal Deposit Insurance Corporation (FDIC)assessments paid on deposits in the United States).Figure 9.1 illustrates how Eurodollar deposit and loan rates, including dollar LIBOR rates, compare with traditional domestic interest rates.

Figure 9.1 US Dollar-Denominated interest rates, June 2005

Note: US Federal Funds Rate 3.00%.

Source: The Financial Times, June 22, 2005, p.23.