9.5 Exchange rate regimes: what lies ahead?

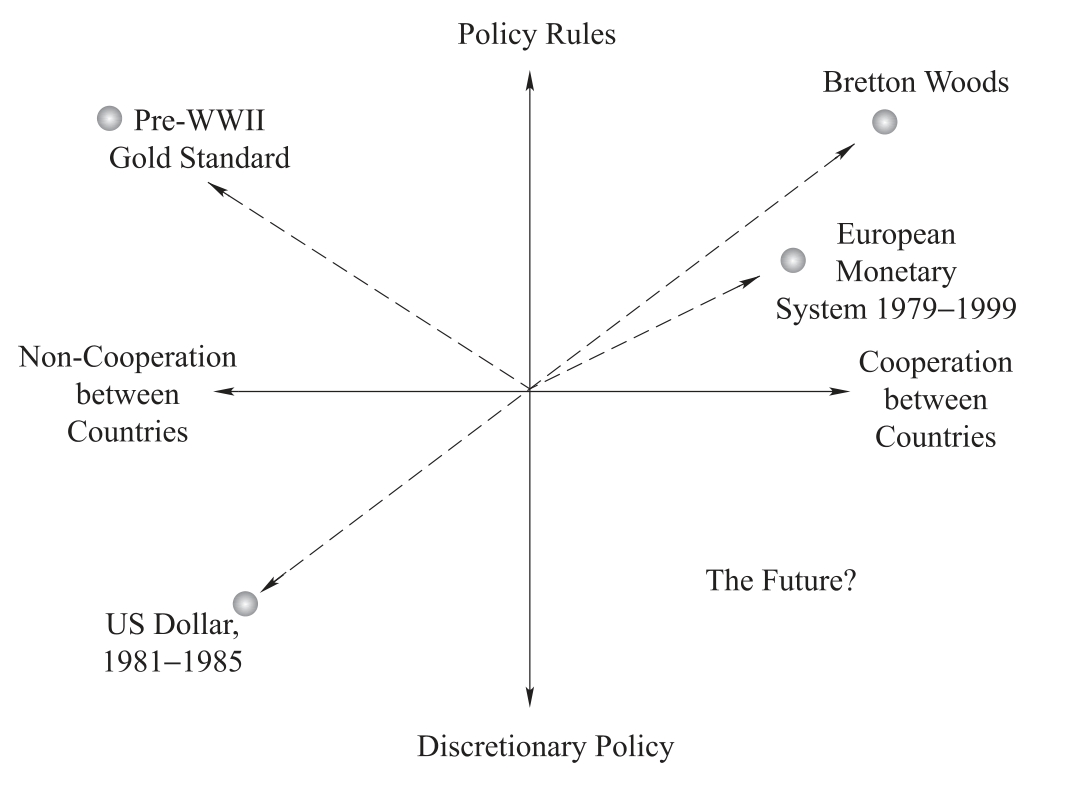

All exchange rate regimes must deal with the trade-off between rules and discretion as well as between cooperation and independence.Figure 9.6 illustrates the trade-offs between exchange rate regimes based on rules, discretion, cooperation, and independence.

● Vertically, different exchange rate arrangements may dictate whether the country’s government has strict intervention requirements—rules—or whether it may choose whether, when and to what degree to intervene in the foreign exchange markets— discretion.

● Horizontally, the trade-off for countries participating in a specific system is between consulting and acting in unison with other countries—cooperation—or operating as a member of the system, but acting on their own—independence.

Figure 9.6 The Trade-offs between exchange rate regimes

Regime structures like the gold standard required no cooperative policies among countries, only the assurance that all would abide by the “rules of the game.” Under the gold standard in effect prior to World War II, this assurance translated into the willingness of governments to buy or sell gold at parity rates on demand.The Bretton Woods Agreement, the system in place between 1944 and 1973, required more in the way of cooperation, in that gold was no longer the “rule”, and countries were required to cooperate to a higher degree to maintain the dollar-based system.Exchange rate systems, like the European Monetary System’s fixed exchange rate band system used from 1979 to 1999, were hybrids of these cooperative and rule regimes.

The present international monetary system is characterized by no rules, with varying degrees of cooperation.Although there is no present solution to the continuing debate over what form a new international monetary system should take, many believe that it could succeed only if it combined cooperation among nations with individual discretion to pursue domestic social, economic and financial goals.

![]()

1.Learn how the international monetary system has evolved from the days of the gold standard to today’s eclectic currency arrangement.

● Under the gold standard (1876-1913), the “rules of the game” were that each country set the rate at which its currency unit could be converted to a weight of gold.

● During the inter-war years (1914-1944)currencies were allowed to fluctuate over fairly wide ranges in terms of gold and each other.Supply and demand forces determined exchange rate values.

● The Bretton Woods Agreement (1944)established a US dollar-based international monetary system.Under the original provisions of the Bretton Woods Agreement, all countries fixed the value of their currencies in terms of gold but were not required to exchange their currencies for gold.Only the dollar remained convertible into gold ($35 per ounce).

● A variety of economic forces led to the suspension of the convertibility of the dollar into gold in August 1971.Exchange rates of most of the leading trading countries were then allowed to float in relation to the dollar and thus indirectly in relation to gold.After a series of continuing crises in 1972 and 1973, the US dollar and the other leading currencies of the world have floated in value since that time.

2.Discover the origin and development of the Eurocurrency market.

● Eurocurrencies are domestic currencies of one country on deposit in a second country.

● Although the basic causes of the growth of the Eurocurrency market are economic efficiencies, a number of unique institutional events during the 1950s and 1960s helped its growth.In 1957, British monetary authorities responded to a weakening of the pound by imposing tight controls on UK bank lending in sterling to nonresidents of the United Kingdom.Encouraged by the Bank of England, UK banks turned to dollar lending as the only alternative that would allow them to maintain their leading position in world finance.For this they needed dollar deposits.Although New York was “home base” for the dollar and had a large domestic money and capital market, international trading in the dollar centered in London because of that city’s expertise in international monetary matters and its proximity in time and distance to major customers.

● Additional support for a European-based dollar market came from the balance of payments difficulties of the United States during the 1960s, which temporarily segmented the US domestic capital market from that of the rest of the world.

3.Analyze the characteristics of an ideal currency.

● If the ideal currency existed in today’s world, it would possess three attributes: a fixed value, convertibility, and independent monetary policy.

4.Explain the currency regime choices faced by emerging market countries.

● Emerging market countries must often choose between two extreme exchange rate regimes, either a free floating regime or an extremely fixed regime such as a currency board or dollarization.

5.Examine how the euro, a single currency for the European Union, was created.

● The 15 members of the European Union are also members of the European Monetary System (EMS).This group has tried to form an island of fixed exchange rates among themselves in a sea of major floating currencies.Members of the EMS rely heavily on trade with each other, so the day-to-day benefits of fixed exchange rates between them are perceived to be great.

● On May 1, 2004, the European Union admitted an additional 10 countries, reaching a total of 25 countries as members.The 10 new members are expected to work toward adoption of the euro gradually over the next six to seven years.

● The euro affects markets in three ways: (1)countries within the euro zone enjoy cheaper transaction costs; (2)currency risks and costs related to exchange rate uncertainty are reduced; and (3)all consumers and businesses both inside and outside the euro zone enjoy price transparency and increased price-based competition.