Settlement procedures

The spreads on the exchange rates that the banks charge their customers are different from the spreads that are found in the inter-bank market.Spreads on the inter-bank market are based on the breadth and depth of a market for a given currency as well as on the currency’s volatility.Currencies that are more volatile or less widely traded usually have higher spreads.Spreads also tend to widen in times of financial or economic turbulence.Because of competition, spreads to bank customers reflect the spreads on the inter-bank market but include a commission.The commission depends on the size of the transaction.Generally speaking, the larger the transaction, the lower the spread.Let’s see what happens in a typical transaction.

On Wednesday, 28 August, 1998, a dollar-based money manager from Renco, a US mutual fund, has USD 1 million that he wants to invest with Barclays in London in a one-year certificate of deposit in Danish krone yielding 10%.A comparable deposit in the United States would only yield 6%.The inter-bank rate is 5.0100-5.0120.The money manager calls around to several banks for quotes without indicating whether he wants to buy or sell krone.The best quote is from Citicorp, at 5.0000-5.0220.Citicorp is taking a commission between the inter-bank bid rate and the rate it is charging the money manager, which works out to 0.2%.For a lower dollar amount the money manager would have had to pay a higher commission.However, he would have paid a lower commission if he had decided to buy the certificate of deposit in a currency that is traded more heavily than the Danish krone.

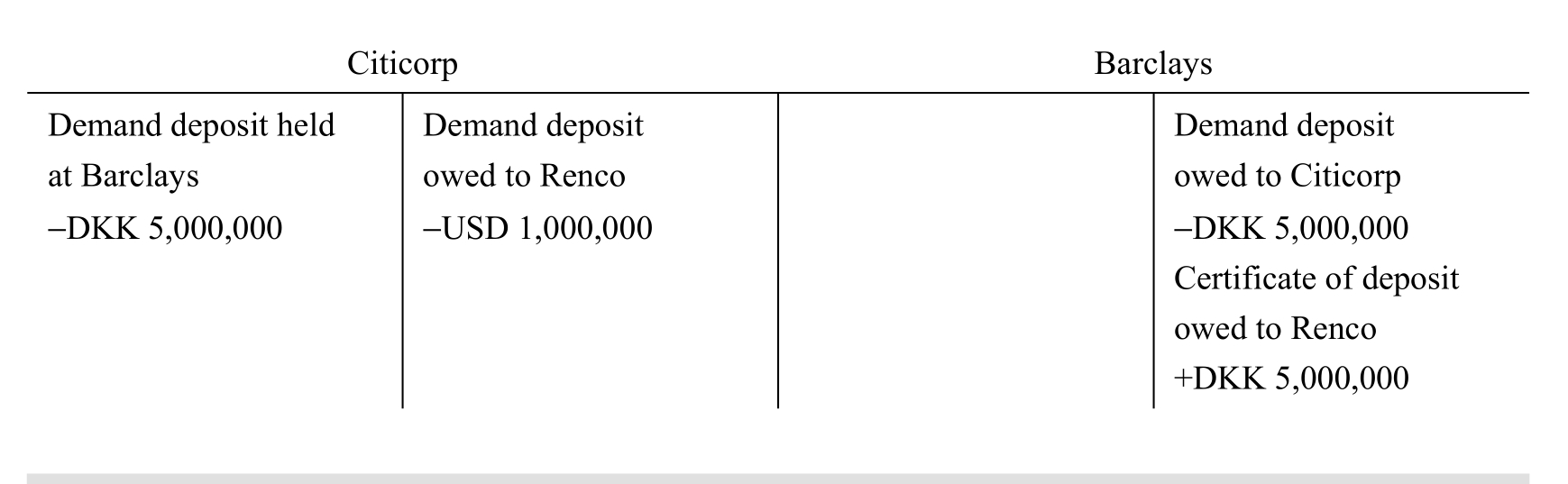

When the agreement is reached between the money manager and Citicorp, telexes are exchanged to confirm.Citicorp requests the details of where the krone are to be paid and Renco gives Citicorp the information on Barclays in London.Citicorp then notifies Barclays on the day of the sale via SWIFT of the impending transfer of Danish krone from Renco.In foreign exchange transactions funds are not usually actually transferred until two business days after the deal was initiated.Thus, two business days later, on Friday 30 August, Citicorp debits Renco’s amount for USD 1 million, Barclays credits Renco’s account for DKK 5 million and Barclays and Citicorp settle between themselves for DKK 5 million.If the transaction had been initiated on Thursday 29 August, the transfer would not have taken place until Monday 2 September, because Saturday and Sunday are not counted as business days.

Recon’s settlement with Barclays is a straightforward bank transaction similar to that in a domestic transaction.The international aspect of the settlement between Citicorp and Barclays, however, makes it worth examining in more detail.It can take two forms.If the two banks maintain correspondent accounts with each other, the transaction described above will be reflected in the banks’ accounts as follows: