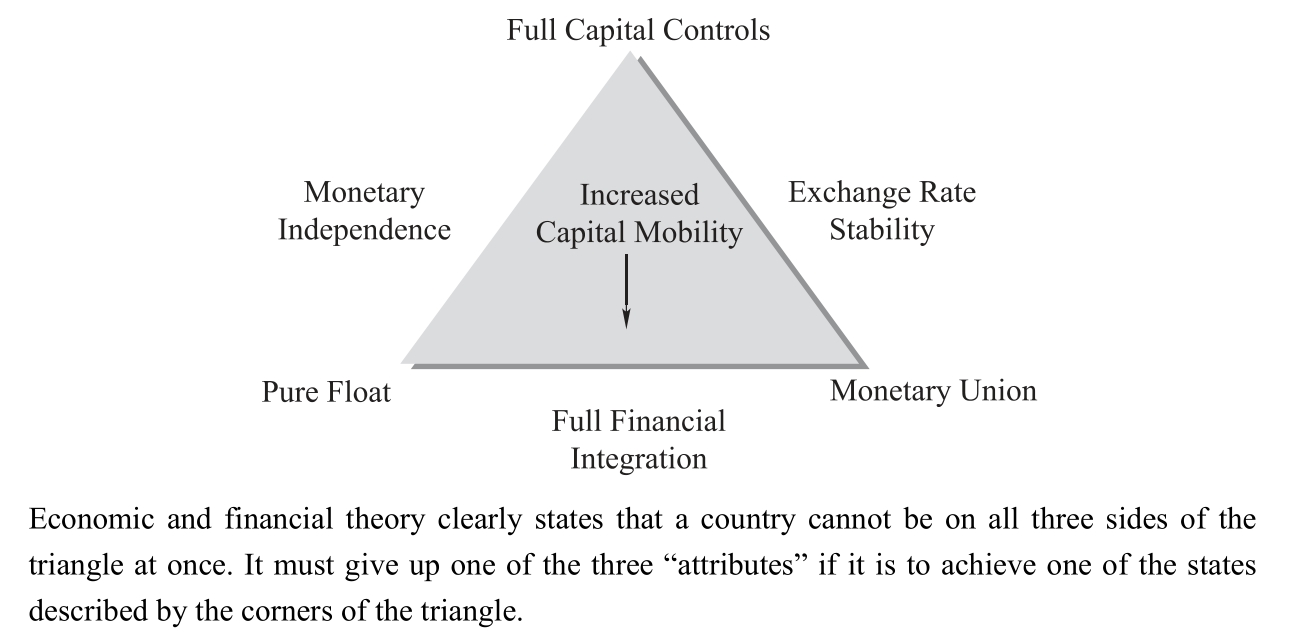

Attributes of the “ideal” currency

If the ideal currency existed in today’s world, it would possess three attributes (illustrated in Exhibit 9.3), often referred to as the “impossible trinity”:

1.Exchange rate stability.The value of the currency would be fixed in relationship to other major currencies, so traders and investors could be relatively certain of the foreign exchange value of each currency in the present and into the near future.

2.Full financial integration.Complete freedom of monetary flows would be allowed, so traders and investors could willingly and easily move funds from one country and currency to another in response to perceived economic opportunities or risks.

3.Monetary independence.Domestic monetary and interest rate policies would be set by each individual country to pursue desired national economic policies, especially as they might relate to limiting inflation, combating recessions, and fostering prosperity and full employment.

These qualities are termed “the impossible trinity” because a country must give up one of the three goals described by the sides of the triangle: monetary independence, exchange rate stability, or full financial integration.The forces of economics do not allow the simultaneous achievement of all three.For example, a country with a pure float exchange rate regime can have monetary independence and a high degree of financial integration with the outside capital markets, but the result must be a loss of exchange rate stability (the case of the United States).Similarly, a country that maintains very tight controls over the inflow and outflow of capital will retain its monetary independence and a stable exchange rate, but at the loss of being integrated with global financial and capital markets (the case of Malaysia in the 1998-2002 period).

As shown in Figure 9.3, the consensus of many experts is that the force of increased capital mobility has been pushing more and more countries toward full financial integration in an attempt to stimulate their domestic economies and feed the capital appetites of their own MNEs.As a result, their currency regimes are being “cornered” into being either purely floating (like the United States)or integrated with other countries in monetary unions (like the European Union).

Figure 9.3 The impossible trinity

Source: Adapted from Lars Oxelheim, International Financial Integration, Springer-Verlag, 1990.P.10.