Hedging with forward contracts

The exposure to be hedged can arise from a commercial transaction, a foreign investment or a liability in foreign currency.It can also be long or short.A position is said to be long when foreign currency or a claim in foreign currency is owned.It is short when there is a liability in foreign currency.For example, an export billed in foreign currency creates a long position for the exporting firm in the form of a claim in foreign currency for the value of the merchandise.On the other hand, an import billed in foreign currency creates a short position for the importing company in the form of a liability for the amount of the purchase.

Hedging a long position

Consider a French cheese company that has just signed a contract for USD 1 million worth of Camembert cheese to be shipped to the United States and paid for in three months time.The spot exchange rate in Paris is:

S0(EUR/USD)bid=1.1000

The treasurer of the company fears a fall in the value of the dollar, which would reduce the company’s income when the cheese is finally delivered and the dollar proceeds are converted into euros.In order to cover this risk his banker suggests that he sell USD 1 million three months forward.The forward rate is:

F0,1/4(EUR/USD)bid=1.1000

This means that no matter what the spot exchange rate is in three months time the company will delivery USD 1 million to the bank and the bank will credit the company’s account for EUR 1.1 million.By selling its dollars forward, the company can guarantee what its income will be in euros.

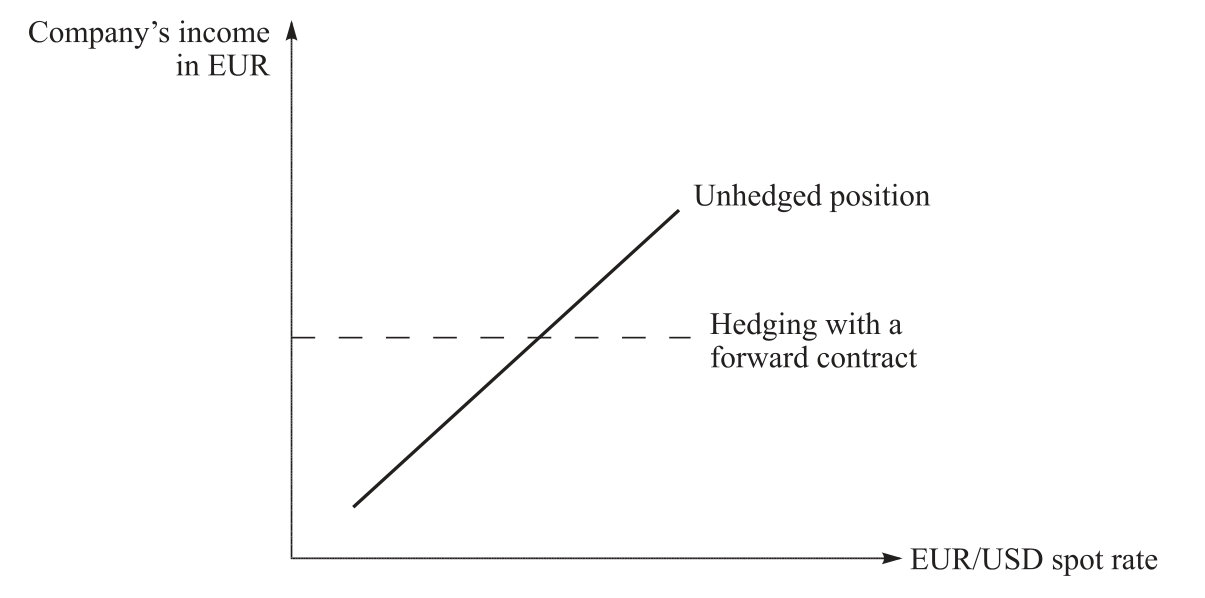

Figure 5.3 illustrates the change in the company’s risk exposure resulting from the forward transaction.The solid line represents the company’s income in euros before making the forward transaction.It depends on the level of the exchange rate.At higher values of the dollar, euro income is higher.At lower dollar values it is lower.The broken line represents the company’s income after the forward transaction.Income in euros is insensitive to the level of the exchange rate.No matter what the value of the dollar, euro income is the same.The forward transaction has effectively eliminated the foreign exchange risk.

Figure 5.3 Hedging a long position

Eliminating foreign exchange risk has disadvantages as well as advantages.The main advantage is that if the value of the dollar falls, the company has no loss of income, which is guaranteed at EUR 1.1 million.The disadvantage is that if the value of the dollar goes up, the company will not benefit from the appreciation.Furthermore, hedging the foreign exchange risk exposes the company to another kind of risk.Suppose that the exporter is not paid on time or that some of his merchandise is refused.The exporter will not have enough dollars to honor his forward contract.In order to make up the difference he will either have to roll over the forward contract at a new rate or buy dollars at the going spot rate.Either rate might be different from the 1.1000 exchange rate of the forward contract.If the rollover rate is lower or the spot ask rate is higher, the company will make an unanticipated loss.Hedging in the forward market is a two-edged sword.

As a general rule of thumb, then, we can say that if the treasurer feels that there is a strong chance that the value of the dollar will fall and a weak chance that it will rise, the treasurer should hedge with a forward contract.In the opposite case where there is a strong chance that the dollar will appreciate and a weak chance that it will depreciate, he should not hedge.

Hedging a short position

Hedging a short position involves buying foreign exchange forward.Consider a French mail order company that has just sign a contract to buy USD 1 million of men’s clothing in three months time from its supplier in Hong Kong Special Administrative Region of China.The current spot exchange rate in Paris is:

S0(EUR/USD)ask=1.1000

The treasurer of the French company fears that the dollar will appreciate and thus raise the cost of the merchandise in euros when the time comes to pay for them.In order to avoid this undesirable eventually, the treasurer goes to the company’s banker and buys USD 1 million three months forward.The forward rate is:

S0(EUR/USD)ask=1.1000

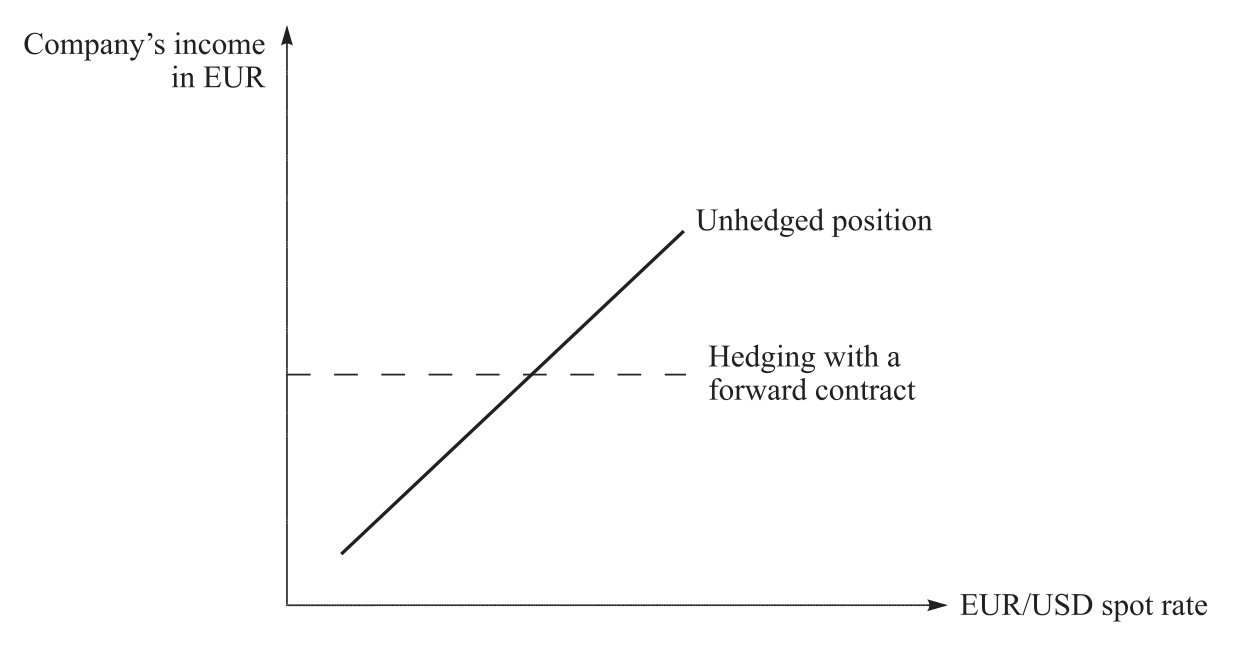

In three months the French company will deliver EUR 1.1 million and receive USD 1 million, no matter what the exchange rate is.Figure 5.4 illustrates the change in the company’s risk exposure resulting from the forward transaction.The solid line represents the company’s expenditure in euros before making the forward transaction.It depends on the level of the exchange rate.At higher values of the dollar, euro expenditure is higher.At lower dollar values it is lower.The broken line represents the company’s expenditure after the forward transaction.Expenditure in euros is insensitive to the level of the exchange rate.No matter what the value of the dollar, euro expenditure is the same.The forward transaction has effectively eliminated the foreign exchange risk.

Figure 5.4 Hedging a short position

Here again, eliminating foreign exchange risk has disadvantages as well as advantages.The key advantage is that if the value of the dollar rises, the company has no increase in expenditure, which is guaranteed at EUR 1.1 million.The disadvantage is that if the value of the dollar goes down, the company will not benefit from the depreciation.Furthermore, as we saw in the preceding example, hedging the foreign exchange risk exposes the company to another kind of risk.Suppose that delivery dates from the company are not respected or that some of the merchandise is not up to standards and must be refused.Expenditure for the merchandise will be lower than expected, which will leave the company with dollar balances once the forward contract is consummated.When the dollar balances are converted back into euros, the spot exchange rate might be higher or lower than the 1.1000 exchange rate of the forward contract.If it is higher the company will make an unanticipated gain.If it is lower it will make an unanticipated loss.This loss of risk would not be present in the absence of the forward contract.

Forward discounts and premiums: long positions

In the foregoing example we have assumed that the forward rate is the same as the current spot rate.While this is possible, it is more likely that the forward rate will be higher or lower than the current spot rate due to the interest rate differential.The existence of a forward premium or discount affects the economics of a hedging transaction.

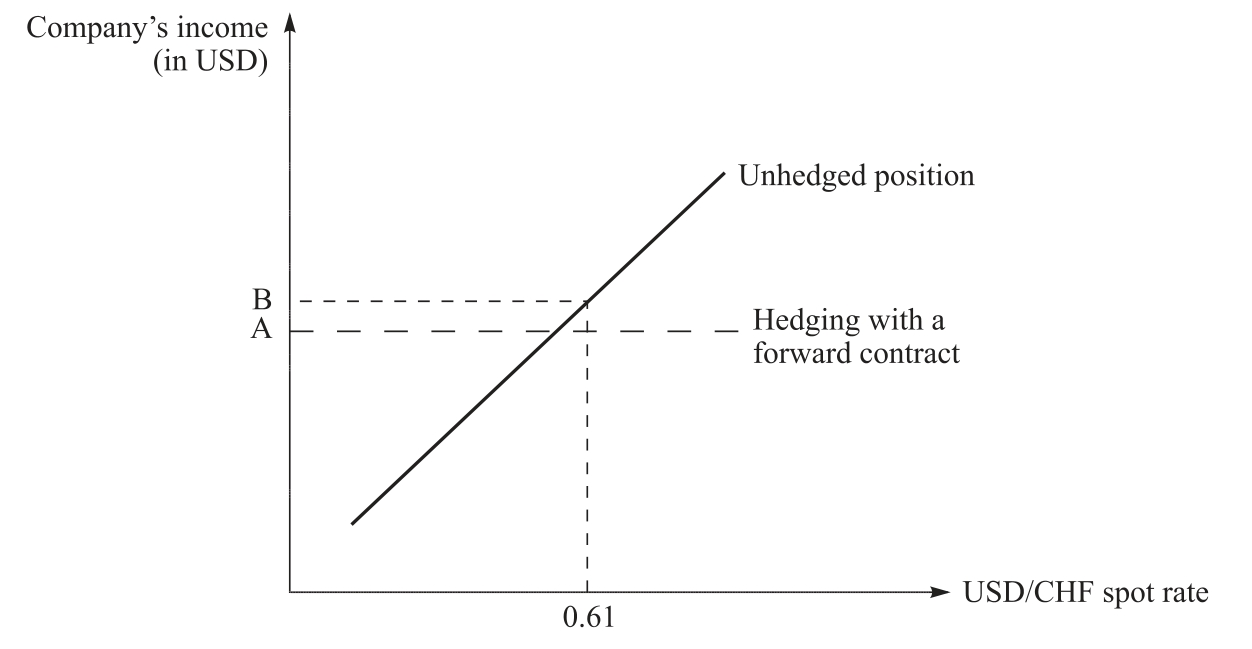

Take the case of a US producer of machine tools that sells to a Swiss importer for delivery and payment in six months and bills the merchandise in Swiss francs.The spot exchange rate in New York is:

S0(USD/CHF)bid=0.6100

But, because Swiss interest rates are higher than US interest rates, the six-month forward rate is:

F0,1/2(USD/CHF)bid=0.6000

a discount of 3.28% on the franc.This means that if the US company hedges its position by selling its franc income forward, its dollar income will be 1.64% lower than it would be at the current spot rate.(Premiums and discounts are quoted in yearly percentages.The yearly discount is 3.28% or 1.64% for six months.)If the US company intends to hedge, the loss of income should be taken into consideration when establishing its price in francs.

Figure 5.5 illustrates the change in the company’s dollar income resulting from the forward transaction.The solid line represents the company’s income in dollars before making the forward transaction.It depends on the level of the exchange rate.At higher values of the dollar, dollar income is lower.At lower dollar values it is higher.The broken line represents the company’s income after the forward transaction.Dollar income is insensitive to the level of the exchange rate.No matter what the value of the dollar, dollar income is the same.However, the dollar income that is locked in is lower by B-A than it would be at the current spot rate.

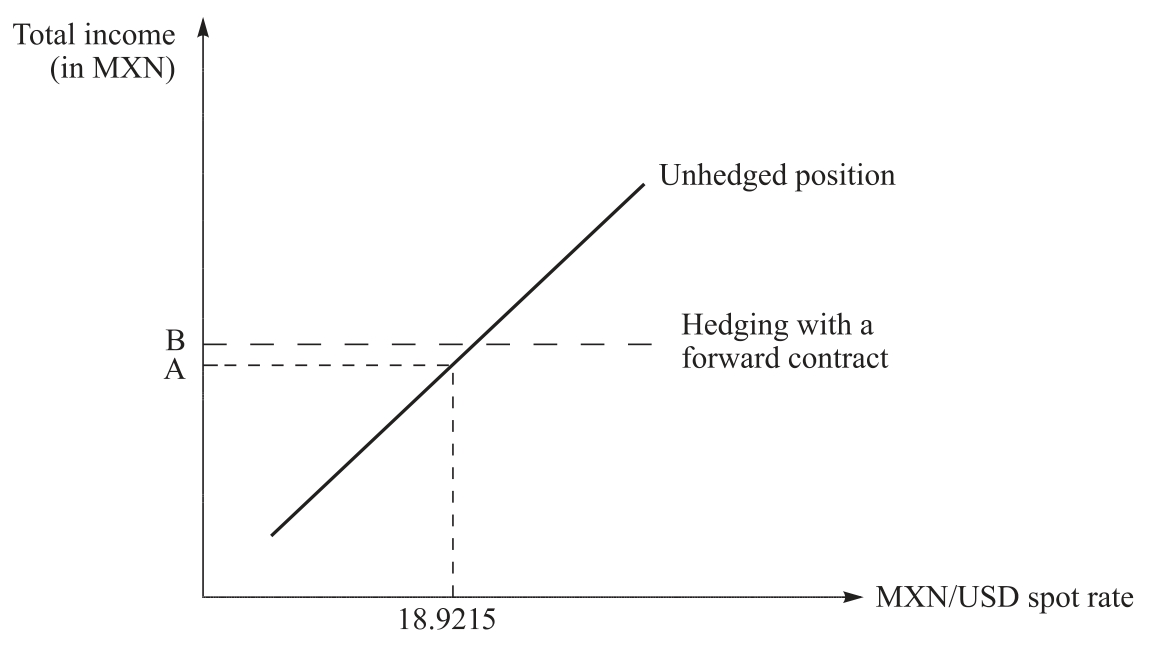

The situation is different when the foreign currency to be received is at a premium.Consider a Mexican exporter of olive oil that makes a sale in the United States for delivery and payment in three months.Commercial expediency dictates that the bill is in US dollars.The spot exchange rate in Mexico is:

S0(MXN/USD)bid=18.9215

Figure 5.5 Hedging a long position with a forward discount

His bank offers him a three-month forward rate of

F0,1/4(MXN/USD)bid=19.1350

a premium of 4.513% (1.128% for three months)on the dollar.

Figure 5.6 illustrates the effect on the company’s peso income resulting from the forward transaction.The solid line represents the company’s income in pesos before making the forward transaction.It depends on the level of the exchange rate.At higher values of the dollar, peso income is higher.At lower values it is lower.The broken line represents the company’s income after the forward transaction.Income in pesos is insensitive to the level of the exchange rate.No matter what the value of the dollar, peso income is the same.However, the premium on the forward dollar makes the peso income that is locked in higher by B-A than what it would be at the current spot rate.The gain resulting from the premium on the dollar should be considered when pricing the merchandise because this is the effective peso income generated by the transaction.

Forward discounts and premiums: short positions

Forward discounts and premiums also influence the economics of short positions.In the case of short positions, a discount is favorable to the hedger because it enables him to obtain foreign exchange at a rate lower than the current spot rate.On the other hand, a premium is unfavorable because it makes forward foreign currency more costly.

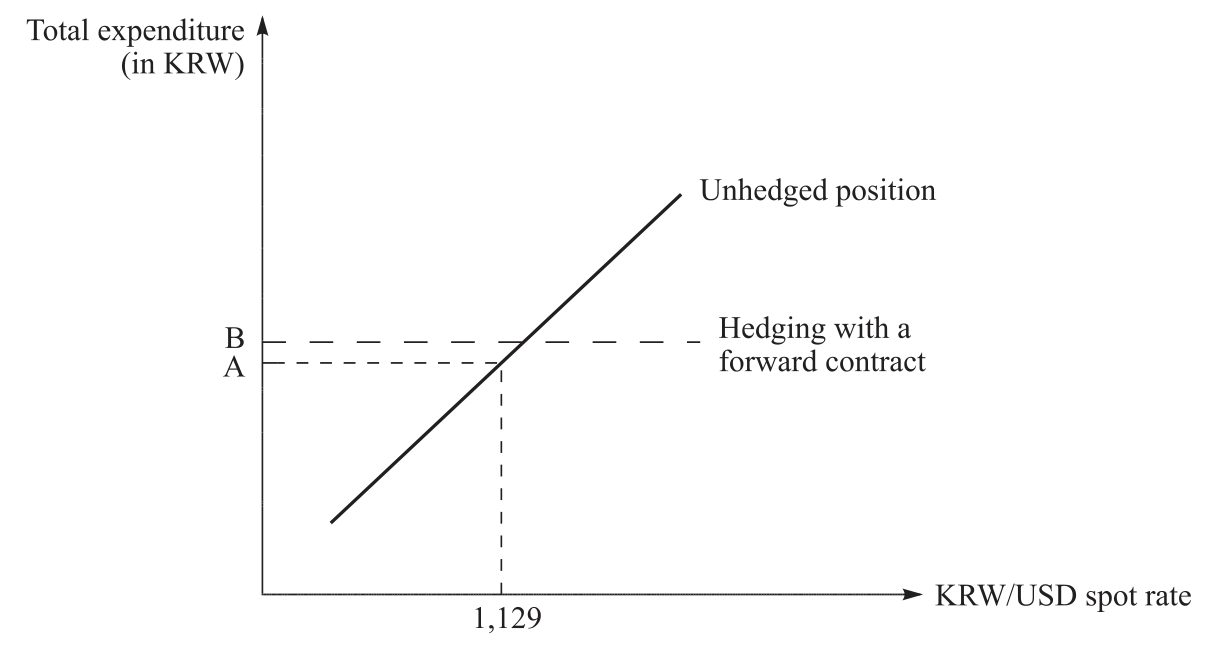

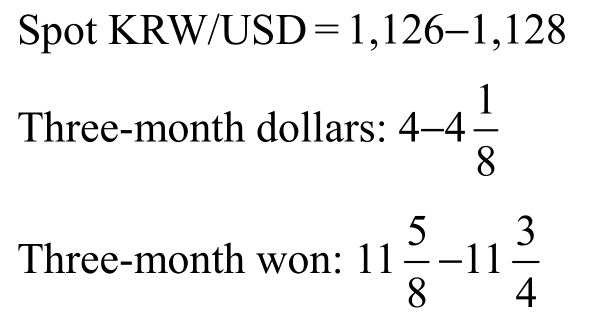

Take, for example, the case of a Korean importer of petroleum products who must pay USD 10 million in three months.He is faced with the following situation:

S0(KRW/USD)ask=1,129

F0,1/4(KRW/USD)ask=1,151

Figure 5.6 Hedging a long position with a forward premium

The dollar is at a premium.Figure 5.7 illustrates the change in the company’s expenditure in won with and without the forward transaction.The solid line represents the company’s expenditure in won if no forward transaction is undertaken.It depends on the level of the exchange rate.At the current spot exchange rate it would be KRW 11.29 billion.The broken line represents the company’s expenditure if the forward transaction is undertaken.At the forward exchange rate it would be KRW 11.51 billion, considerably higher than at the current spot rate.Buying forward effectively eliminates the exchange risk but it increases the cost.Thus, if the company hedges, the price it charges its customer should be calculated on the forward rate and not the current spot rate.If it doesn’t hedge, of course, it won’t know what its cost is until it actually pays for the merchandise.

Figure 5.7 Hedging a short position with a forward premium

Hedging via the spot market

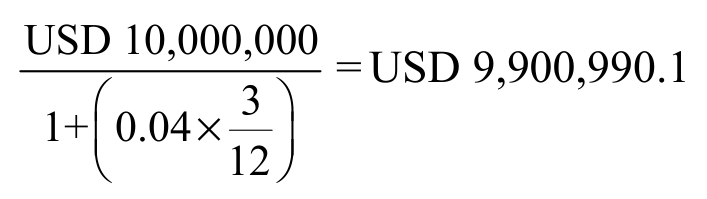

Hedging a future income or expenditure in foreign currency can be achieved without using the forward market.It involves borrowing or lending and then using the spot market.Going back to the Korean importer of petroleum products, for example, we know he could have eliminated his foreign exchange risk by using won to buy spot dollars and then lending his dollars until payment was due when he would use the dollars from the loan to pay off the merchandise.However, since the Korean importer’s business is petroleum products and not financial arbitrage, he would probably not want to tie his money up in this way.Insofar as arbitrage ensures that both routes are equivalent, he would let the bank do the work and use the forward market.

When the bank makes a forward contract, it exposes itself to foreign exchange risk just like any other enterprise.Suppose that the inter-bank exchange rate and interest rates are:

In order to hedge its position with the Korean exporter, the bank will buy dollars spot at KRW 1,128 per dollar and lend the dollars for three months at 4% per year.The bank needs to deliver USD 10 million to the Korean importer in three months.Thus, it will buy

And pay

USD 9,900,990.11128 KRW/USD=KRW 11,168,000,000

It can finance the dollar purchase by borrowing KRW 11.168 billion at 11.75% for three months.At the end of three months it will pay

Thus, the bank would be fully hedged if it charged a forward rate of KRW 1,149.61 (KRW 11.49606 billion USD 10 million).At the rate of 1,151, its profit will be the difference between the KRW 11.51 billion it will receive from the forward transaction and the KRW 11.49606 billion to pay off the loan.

Rolling over and closing out forward contracts

Expected inflows or outflows of foreign currency are not always realized.When this happens, the company can ask its bank to roll the forward contract over or to make a partial settlement and roll over the difference.The procedure is straightforward and is equivalent to closing out the old forward contract and making a new one.

Take the case of an Israeli company that bought USD 1 million three months forward at the end of June at ILS 5.0860 (shekels)for one USD.At the end of September, the merchandise that it ordered still has not been shipped, so the treasurer calls his bank and asks to roll the forward contract over for two months.On the day he calls, the spot ask rate is 5.1500 and the two-month forward premium on the dollar is 765.The new forward rate is thus 5.1500+0.0765=5.2265.However, the company has made a profit on the difference between the current spot rate and the old forward rate equal to

5.1500-5.0860=0.064

The effective rate that the company will pay for the dollars after the forward contract is rolled over is equal to the new forward rate less the profit on the old forward contract:

5.2265-0.064=5.1625

It is higher than the 5.0860 that it would have paid had the merchandise been shipped on time but it is lower than the 5.2265 that it would have had to pay if there had been no forward cover at all.

In accounting for rollover transactions, banks have several possibilities.They can debit the company’s account for ILS 5,086,000 from the forward transaction and simultaneously credit the account for ILS 5,150,000 as a resale of the currency.Then two months later they debit the account for ILS 5,226,500 and credit for USD 1,000,000 for a net cost of ILS 5,162,500.An alternative is to make no entries at the time of the rollover and at maturity to debit the company’s account at a rate equal to the rate on the old forward contract plus the new premium (or discount):

5.0860+0.0765=5.1625

Whatever method is chosen, the cost to the company will be the same.

A company can also terminate a forward contract before maturity.Suppose that for some reason a foreign currency that was expected in three months is actually paid at the end of two months.The company can terminate the forward contract by buying the foreign currency one month forward to offset the ongoing forward three-month contract.It then sells the currency it has received on the spot market.