Interest rate swaps

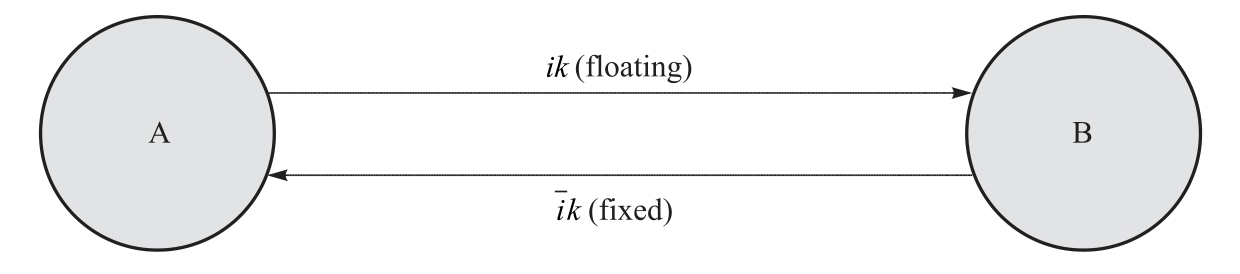

The basic kind of interest rate swap, called a fixed-for-floating swap, involves the exchange of a notional principal valued at fixed and floating (variable)interest rates denominated in the same currency.Figure 7.1 shows two counterparties, A and B, involved in such a swap, whereby A receives payments based on a fixed rate and B receives payments based on a floating rate (such as LIBOR), both of which are calculated on the basis of a notional principal that is never exchanged, k.Thus, on each payment date, A receives ik whereas B receives ik, where  and i are the fixed and floating interest rates, respectively.In practice, net compensatory payments are made by one counterparty to the other, depending on whether the floating rate turns out to be higher or lower than the fixed rate.If the floating interest rate turns out to be higher than the fixed interest rate, then B must receive a net compensatory payment from A.this payment is equal to the difference between the two rates applied to the notional principal, k (i-

and i are the fixed and floating interest rates, respectively.In practice, net compensatory payments are made by one counterparty to the other, depending on whether the floating rate turns out to be higher or lower than the fixed rate.If the floating interest rate turns out to be higher than the fixed interest rate, then B must receive a net compensatory payment from A.this payment is equal to the difference between the two rates applied to the notional principal, k (i- ).If, on the other hand, the fixed rate turns out to be higher, A must receive k (

).If, on the other hand, the fixed rate turns out to be higher, A must receive k ( -i).

-i).

Figure 7.1 Fixed-for-floating interest rate swaps

Other kinds of interest rate swaps include the basis swap and the zero-coupon swap.A basis involves two variable interest rates, such as the deposit rate and the rate on Treasury bills.A zero-coupon swap involves a zero fixed rate, in which case the receiver of the payment based on the fixed rate receives everything on the maturity of the contract.