Exercises

1.Single-choice questions

(1)If you think that the dollar is going to appreciate against the euro,____________.

a.you should buy put options on the euro

b.you should sell call options on the euro

c.you should buy call options on the euro

d.None of the above.

(2)From the perspective of the writer of a put option written on €62,500.If the strike price is $1.25/€, and the option premium is $1,875, at what exchange rate do you start to lose money?

a.$1.22/€ b.$1.25/€ c.$1.28/€ d.None of the above.

(3)A European option is different from an American option in that____________.

a.one is traded in Europe and one in traded in the United States

b.European options can only be exercised at maturity; American options can be exercised prior to maturity

c.European options tend to be worth more than American options, ceteris paribus

d.American options have a fixed exercise price; European options’ exercise price is set at the average price of the underlying asset during the life of the option

(4)An “option” is____________.

a.a contract giving the seller (writer)the right, but not the obligation, to buy or sell a given quantity of an asset at a specified price at some time in the future

b.a contract giving the owner (buyer)the right, but not the obligation, to buy or sell a given quantity of an asset at a specified price at some time in the future

c.not a derivative, nor a contingent claim, security

d.unlike a futures or forward contract

(5)An investor believes that the price of a stock, say IBM’s shares, will increase in the next 60 days.If the investor is correct, which combination of the following investment strategies will show a profit in all the choices?

(i)—buy the stock and hold it for 60 days

(ii)—buy a put option

(iii)—sell (write)a call option

(iv)—buy a call option

(v)—sell (write)a put option

a.(i), (ii), and (iii) b.(i), (ii), and (iv)

c.(i), (iv), and (v) d.(ii)and (iii)

(6)Most exchange traded currency options____________.

a.mature every month, with daily resettlement

b.have original maturities of 1, 2, and 3 years

c.have original maturities of 3, 6, 9, and 12 months

d.mature every month, without daily resettlement

(7)The volume of OTC currency options trading is____________.

a.much smaller than that of organized-exchange currency option trading

b.much larger than that of organized-exchange currency option trading

c.larger, because the exchanges are only repackaging OTC options for their customers

d.None of the above.

(8)Exercise of a currency futures option results in____________.

a.a long futures position for the call buyer or put writer

b.a short futures position for the call buyer or put writer

c.a long futures position for the put buyer or call writer

d.a short futures position for the call buyer or put buyer

(9)Swap transactions____________.

a.involve the simultaneous sale (or purchase)of spot foreign exchange against a forward purchase (or sale)of approximately an equal amount of the foreign currency

b.account for about half of Interbank FX trading

c.All of the above.

d.involve trades of one foreign currency for another without going through the US dollar

(10)As a rule, when the interest rate of the foreign currency is greater than the interest rate of the quoting currency,____________.

a.the outright forward rate is less than the spot exchange rate

b.the outright forward rate is more than the spot exchange rate

c.the currency will trade at a premium in the forward contract

d.None of the above.

(11)Bank dealers in conversations among themselves use a shorthand notation to quote bid and ask forward prices in terms of forward points.This is convenient because____________.

a.forward points may change faster than spot and forward quotes

b.in swap transactions where the trader is attempting to minimize currency exposure the actual spot and outright forward rates are often of no consequence

c.it’s cool to look smart around your peers

d.time is money

(12)A________exchange contract is an agreement to exchange one currency for another on some date in the future at a price set now.

a.spot domestic b.forward domestic

c.spot foreign d.forward foreign

(13)________means committing oneself to an uncertain future value of one’s net worth in terms of home currency.

a.Selling b.Hedging

c.Speculating d.Importing

(14)Assume you are a Chinese exporter and expect to receive $250,000 at the end of 60 days.You can remove the risk of loss due to a devaluation of the dollar by____________.

a.selling dollars in the forward market for 60-day delivery

b.buying dollars now and selling it at the end of 60 days

c.selling the yuan equivalent in the forward market for 60-day delivery

d.keeping the dollars in the United States after they are delivered to you

(15)Assume you are an American importer who must pay 500,000 euros at the end of 90 days when you receive 1,000 cases of French wine at your warehouse in New York.If you do not cover this transaction in the forward market, you face a risk of loss if the euro____________.

a.depreciates against the dollar

b.appreciates against the dollar

c.either appreciates or depreciates against the dollar

d.is fixed

(16)Assume you are an American importer who must pay 500,000 euros at the end of 90 days when you receive 1,000 cases of French wine at your warehouse in New York.If you do not hedge this transaction, you face exchange rate risk.The best way to remove the risk of loss due to currency fluctuations is to____________.

a.buy 500,000 euros in the forward market for delivery in 60 days

b.buy 500,000 euros now, hold them for 60 days, and then sell them at the current spot rate

c.sell 500,000 euros in the forward market for delivery after 60 days

d.sell 500,000 euros now in the spot market

(17)An import-export business that finds itself in a “short” foreign-currency position risks a financial loss if____________.

a.exports fall b.domestic currency appreciates

c.domestic currency depreciates d.foreign currency depreciates

(18)In a________contract you can effectively lock in the price at which you buy or sell a foreign currency at a set date in the future.

a.securities spot b.securities futures

c.currency futures d.spot foreign exchange

(19)Which financial instrument provides a buyer the right (but not the obligation)to purchase or sell a fixed amount of currency at a prearranged price, within a few days to a couple of years?

a.Letter of credit. b.Foreign currency option.

c.Currency swap. d.Forward contract.

(20)For an investor who starts with dollars and wants to end up with dollars in the future, which of the following choices is an example of hedging?

a.Sell dollars at the spot rate, invest the proceeds in foreign currency-denominated financial instruments, and sign a forward exchange contract to buy the foreign currency.

b.Sell dollars at the spot rate, invest the proceeds in foreign currency-denominated financial instruments, and sign a forward exchange contract to buy dollars.

c.Sell dollars at the spot rate, invest the proceeds in foreign currency-denominated financial instruments, and then buy dollars at the future spot rate.

d.Buy a dollar-denominated financial asset.

(21)If the spot price of the euro is $1.10 per euro and the 30-day forward rate is $1.00 per euro, and you believe that the spot rate in 30 days will be $1.05 per euro, you can maximize speculative gains by____________.

a.buying euros in the spot market and selling the euros in 30 days at the future spot rate

b.signing a forward foreign exchange contract to sell the euros in 30 days

c.signing a forward foreign exchange contract to sell the dollars in 30 days

d.buying dollars in the spot market and selling the dollars in 30 days at the future spot rate

2.True/False questions

(1)Hedging a position exposed to exchange rate risk is the act of reducing or eliminating a net asset or net liability position in the foreign currency.

(2)Speculating in a position exposed to exchange rate risk is the act of reducing or eliminating a net asset or net liability position in the foreign currency.

(3)The profits and losses on a futures contract accrue to you daily, as the contract is “marked to market” daily.

(4)Forward exchange contracts are used for hedging but not for speculating.

(5)In a currency swap two parties agree to exchange flows of different bonds during a specified period of time.

(6)If a currency is at a forward premium by as much as its interest rate is lower than the interest rate in the other country, covered interest parity holds.

(7)A country with an interest rate that is lower than the corresponding rate in the domestic country will have a forward premium on its currency.

(8)Covered interest parity is rarely found to hold empirically.

(9)If Canada and Britain have 90 day forward exchange rate values for their currencies that are above their current spot exchange rate values, then Canadian and British interest rates are relatively high.

(10)Studies have shown that actual uncovered differentials are random and on average equal to zero.

(11)The forward contract can hedge future receivables or payables in foreign currencies to insulate the firm against exchange rate risk.

(12)A put option is an option to sell-by the buyer of the option-a stated number of units of the underlying instrument at a specified price per unit during a specified period.

(13)Futures must be marked-to-market.Options are not.

(14)Speculators who expect a currency to appreciate could purchase currency futures contracts for that currency.

(15)The option writer is obligated to buy the underlying commodity at a stated price if a put option is exercised.

3.Essay questions

(1)What is interest rate swap?

(2)The current spot exchange rate is $1.14/Euro.The current 90-day forward exchange rate is $1.11/Euro.How could a US firm, who must repay a 40 million Euro loan in 90 days, use a forward exchange contract to hedge its risk exposure?

(3)A US company ordered a Jaguar sedan.In 6 months, it will pay £30,000 for the car.It worried that pound sterling might rise sharply from the current rate($1.90).So, the company bought a 6 month pound call (supposed contract size = £35,000)with a strike price of $1.90 for a premium of 2.3 cents/£.

a.Is hedging in the options market better if the £ rose to $1.92 in 6 months?

b.what did the exchange rate have to be for the company to break even?

(4)The strike price for a call is $1.67/£.The premium quoted at the Exchange is $0.0222 per British pound.

Diagram the profit and loss potential, and the break-even price for this call option.

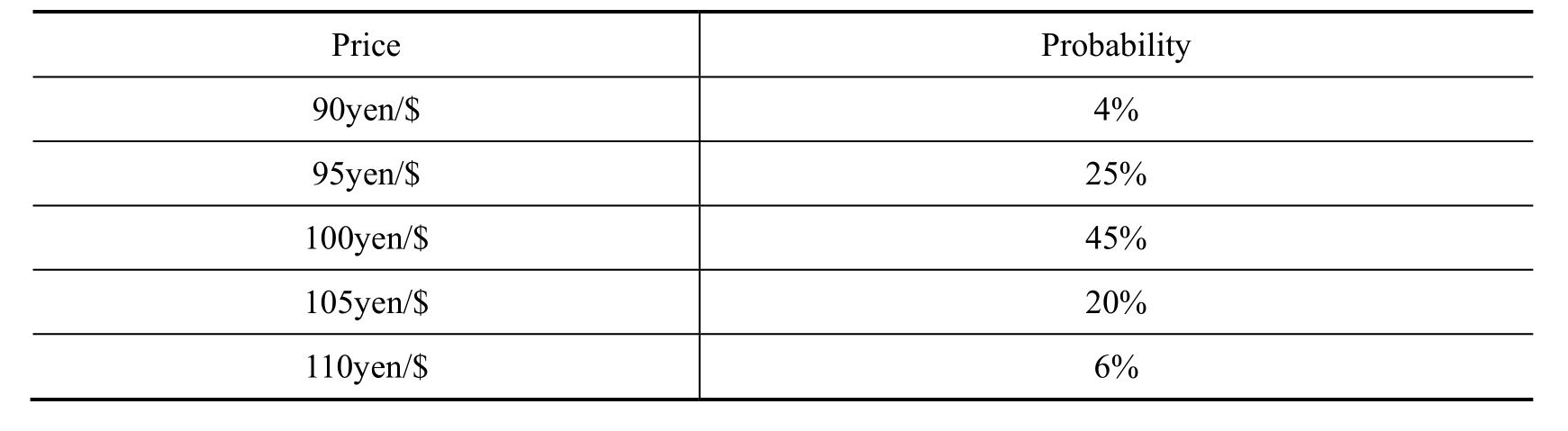

(5)Suppose that you are expecting revenues of 100,000 yen from Japan in one month.Currently, 1 month forward contracts are trading at $1 = 105 yen.You have the following estimate of the yen/$ exchange rate in one month.

a.What position in forward contracts would you take to hedge your exchange risk?

b.Calculate the expected value of the hedge.

c.How could you replicate this hedge in the money market?

(6)In what ways does a currency futures contract differ from a forward currency contract?