Quotes and spreads

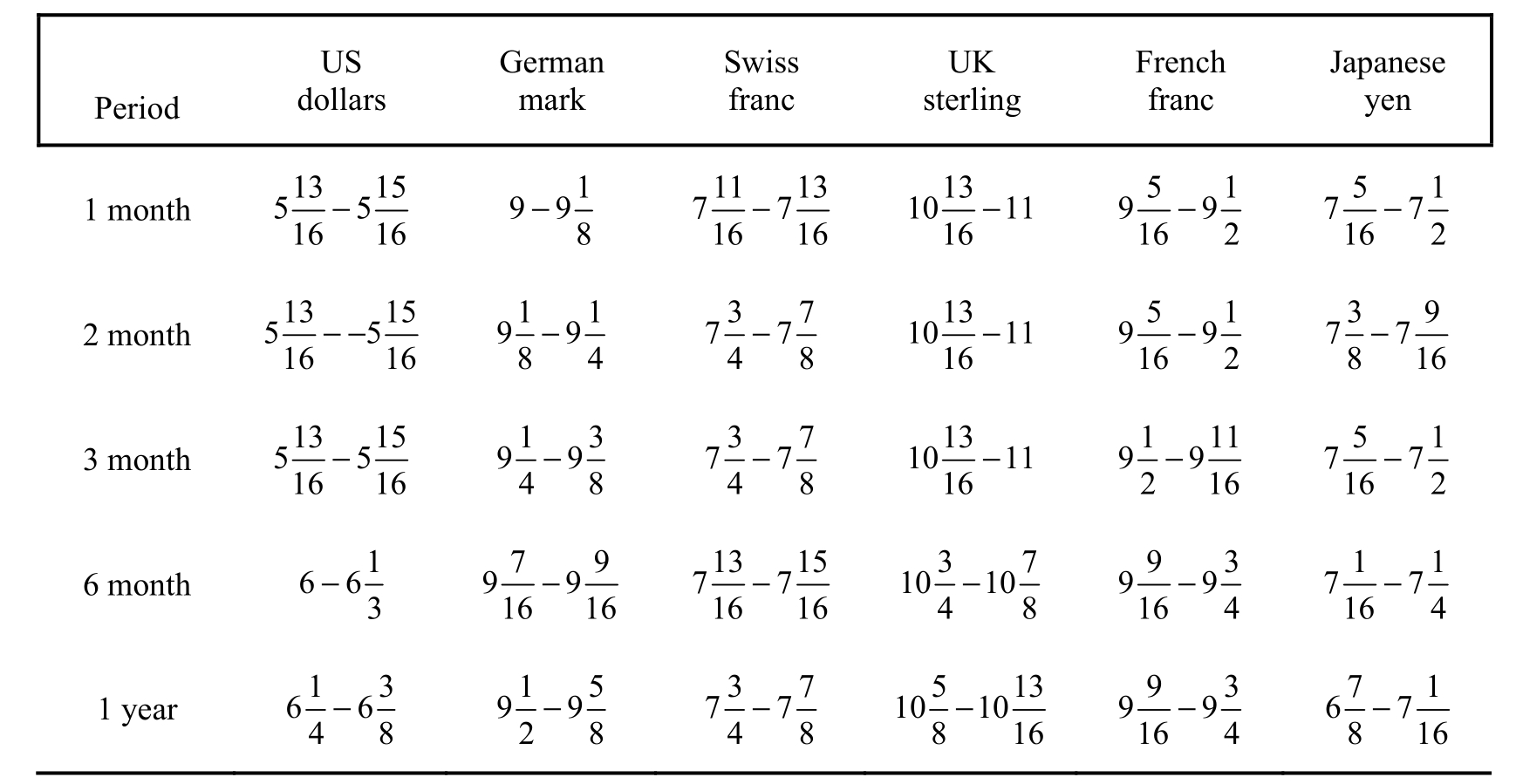

Table 10.2 shows some Eurocurrency interest rates as reported in the International Herald Tribune.These rates refer to the interbank market and are quoted as a bid-ask spread.For example, the interest rate on six-month Eurosterling is quoted![]() .The first figure,

.The first figure, ![]() refers to the rate that banks are willing to pay another bank to borrow sterling for six months.The second figure,

refers to the rate that banks are willing to pay another bank to borrow sterling for six months.The second figure, ![]() refers to the rate that banks charge to lend sterling to another bank for six months.The difference of

refers to the rate that banks charge to lend sterling to another bank for six months.The difference of ![]() % between the two rates, the spread, is the banks’ gain.

% between the two rates, the spread, is the banks’ gain.

Table 10.2 Eurocurrency interest rates

Source: International Herald Tribune (5 August 1991).

Note: Rates applicable to interbank deposits of USD 1 million minimum (or equivalent).

If a trader gives a quotation such as the 10 above, it means that his bank is ready to borrow from, or lend to, any institution of good standing at those rates.Table 10.2 indicates that the rates shown refer to deposits of USD 1 million or the foreign exchange equivalent, which is the usual minimum transaction size in the interbank market.Banks generally set maximums to limit their risks.

above, it means that his bank is ready to borrow from, or lend to, any institution of good standing at those rates.Table 10.2 indicates that the rates shown refer to deposits of USD 1 million or the foreign exchange equivalent, which is the usual minimum transaction size in the interbank market.Banks generally set maximums to limit their risks.

A non-member of the interbank club, such as a corporation or investor wishing to lend into this market, will be given a quote of the bid rate less a commission.Because of fierce competition among banks, commissions on lending are typically very low.In the example above, if the commission is ![]() , a customer would be able to lend six-month sterling to the bank at

, a customer would be able to lend six-month sterling to the bank at ![]() less

less ![]() On the other hand, a customer wishing to borrow from the market will be quoted the ask or offer rate plus a commission that includes a risk premium.The risk premium depends on the customer’s credit worthiness.The more doubtful the customer’s credit worthiness, the higher the premium.A good quality customer might be able to borrow at

On the other hand, a customer wishing to borrow from the market will be quoted the ask or offer rate plus a commission that includes a risk premium.The risk premium depends on the customer’s credit worthiness.The more doubtful the customer’s credit worthiness, the higher the premium.A good quality customer might be able to borrow at ![]() % over the ask rate.In the example above the customer would then have to pay

% over the ask rate.In the example above the customer would then have to pay  Quotes for Eurocurrency loans are often given in terms of Libor (London interbank offered rate)or Pibor (Paris interbank offered rate)plus the risk-adjusted commission.Libor rates are calculated as the averages of the lending rates in the respective currencies of six leading London banks.Pibor rates are the averages of the lending rates of the 14 top Parisian banks in the respective currencies where the three highest and the three lowest rates are eliminated.

Quotes for Eurocurrency loans are often given in terms of Libor (London interbank offered rate)or Pibor (Paris interbank offered rate)plus the risk-adjusted commission.Libor rates are calculated as the averages of the lending rates in the respective currencies of six leading London banks.Pibor rates are the averages of the lending rates of the 14 top Parisian banks in the respective currencies where the three highest and the three lowest rates are eliminated.

For borrowing maturities of over a year, a “floating” interest rate is usually charged.Floating interest rates mean that periodically (every six months, for example)the loan is rolled over and the interest rate is revised according to current Libor.In the example above, suppose that the customer negotiated a five-year sterling loan at Libor plus ![]() % revisable every six months.As we saw, he would have to pay

% revisable every six months.As we saw, he would have to pay ![]() % for the first six months.Suppose that at the end of six months sterling rates have fallen so that six-month sterling Libor is at

% for the first six months.Suppose that at the end of six months sterling rates have fallen so that six-month sterling Libor is at ![]() %.The customer will then have to pay

%.The customer will then have to pay ![]() for the next six months.

for the next six months.

It is interesting to note that Libor and Pibor are losing some of their importance as the benchmarks for lending in the Euromarket.This is because as a result of bad management and bad loans, banks themselves are perceived as inferior credit risks to many other borrowers.These borrowers can borrow at rates below Libor and Pibor and thus bypass the banks.The rapid growth of the Eurobond market, which we will examine in a later chapter, can be attributed to this phenomenon.