3.2 The Mundell-Fleming model

This model owes its origins to papers published by James Fleming (1962)and Robert Mundell (1962, 1963).Their major contribution was to incorporate international capital movements into formal macroeconomic models based on the Keynesian IS-LM framework.Their papers led to some dramatic implications concerning the effectiveness of fiscal and monetary policy for the attainment of internal and external balance.We shall now examine the main implications of the Keynesian model and the results of Fleming’s and Mundell’s papers by using what is known as IS-LM-BP analysis.

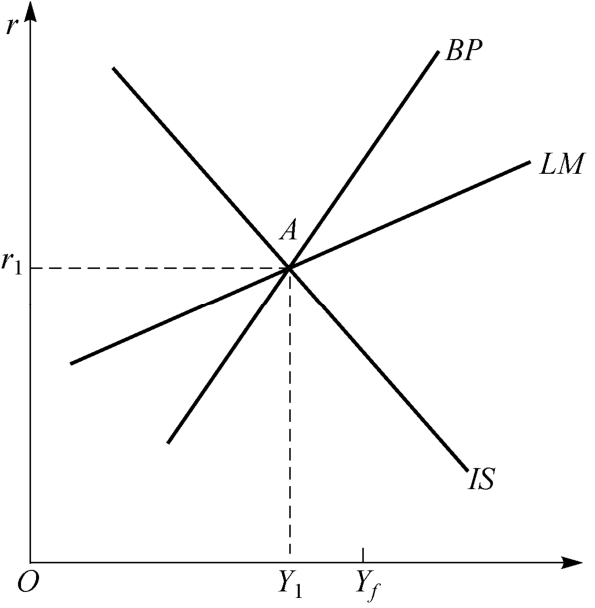

Figure 3.2 depicts all three schedules intersecting through a common point.The BP schedule is steeper than the LM schedule, but this need not always be the case.As we shall see later, changing the relative slope of the two schedules can lead to somewhat different policy prescriptions.All three schedules pass through a common point A which corresponds to the domestic interest rate r1 and income level Y1.The income level Y1 is seen to be less than that of the full employment level of income Yf, implying that there is some unemployment in the economy.Although the economy is not in internal equilibrium, the balance of payments is in equilibrium because the IS and LM schedules intersect at a point on the BP schedule.

Figure 3.2 Equilibrium of the model

The explanation as to why the IS-LM schedules do not intersect at the full employment level of income Yf is that at Yf planned leakages (savings and import expenditure)would exceed planned injections (government expenditure, exports and investment).This would imply a build-up of stocks of unsold goods leading producers to reduce output.Only at output level Y1 do planned leakages equal planned injections so that changes in stocks are avoided.

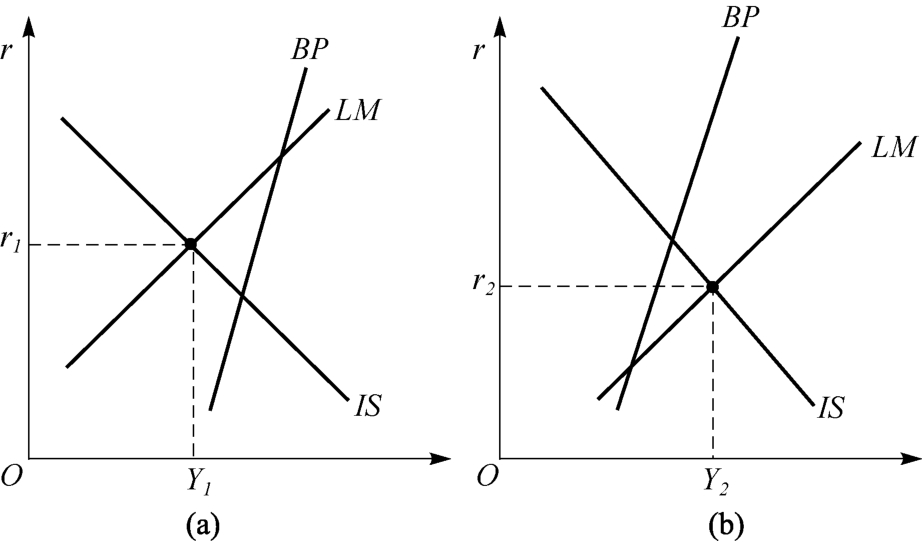

In Figure 3.3(a)and Figure 3.3(b)we depict scenarios where there is a surplus and deficit respectively in the balance of payments.In Figure 3.3(a)because the IS and LM schedules intersect to the left of the BP schedule there is a balance-of-payments surplus.This surplus comes about because the level of income is too low and/or the rate of interest is too high to be compatible with overall equilibrium.In Figure 3.3(b)there is a balance-of-payments deficit because the IS and LM schedules intersect to the right of the BP schedule; this means that the income level Y2 is too high and/or interest rate r2 too low, inducing an overall balance-of-payments deficit.

Figure 3.3 Surplus (a)and deficit (b)in the balance of payments

In the analysis of the rest of this chapter we need to consider how changes in the exchange rate and monetary and fiscal policies affect the position of the various schedules.