Cross-currency interest rate swaps

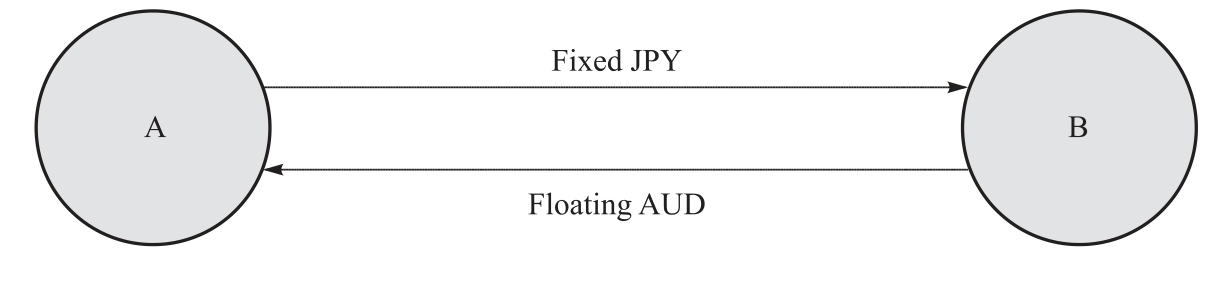

A cross-currency interest rate swap involves the exchange of payments in different currencies.One set of payments is calculated on the basis of a fixed interest rate, whereas another is calculated on the basis of a variable interest rate.This arrangement can be executed as a single transaction between two counterparties, A and B.Figure 7.2(a)illustrates a swap whereby A receives floating interest Australian dollar payments and B receives fixed interest Japanese yen payments.Figure 7.2(b)shows that counterparty A deals with two counterparties to separate the cross-currency and interest rate components.A pays C the fixed Australian dollar payments received from B, in return for floating Australian dollar payments.

Figure 7.2 (a) Dealing with one counterparty

Figure 7.2 (b) Dealing with two counterparties

![]()

1.Futures contracts emerged in response to three problematic characteristics of forward contracts: (i)non-standardization of the contracts; (ii)risk of default; (iii)lack of liquidity.

2.Futures markets perform two important functions: price discovery and risk transfer.

3.A currency swap, which is different from a foreign exchange swap, is a transaction in which two counterparties exchange specific amounts of two different currencies at the outset and repay over time in accordance with a predetermined rule that reflects both interest payments and the amortization of principal.Currency swaps have evolved as a successor to parallel loans.