The forward foreign exchange market

Spot exchange rates are quoted for delivery two business days after the transaction is concluded.Foreign exchange traders in the inter-bank market also quote exchange rates for delivery further than two days in the future.Deals like this are called forward contracts.The rates and the amount are agreed on today but settlement occurs sometime later than two days in the future.Contracts can be negotiated for just about any maturity but most banks supply regular quotes on maturities of 30, 60, 90, and 180 days.

Forward quotes

● Discounts and premiums

When we looked at interest parity we established the relationship between the spot and forward exchange rates and the interest rate differential.Equation (6.1)reproduced here for convenience, stated that relationship:

We said that the left-hand side of the equation represented the forward premium or the forward discount.It is useful, as we shall see, to present the premium or discount as an annual percentage in order to compare it with interest rates which are also presented this way.This can be done by dividing the discount by the number of years or fraction of a year of the forward contract’s duration:

where t represents the number of years to the contract’s settlement.Thus F0,1 means the contract will be settled in one year, F0,2 means it will be settled in two years and F0,1/4 means the contract will be settled in one-fourth of a year or 90 days.

Let’s take a simple example where no transaction costs are involved.Suppose that the Won (KRW)spot rate versus the dollar is KRW 1,308.00 and that the forward rate for delivery 90 days later is KRW 1,327.50.On a 360-day year basis, 90 days is one-quarter of one year.We can apply Formula (6.3)to calculate the premium as an annual percentage that must be paid in South Korean won to buy one dollar today for delivery 90 days in the future:

Thus, it will cost 5.96% more won to buy a dollar for delivery 90 days forward than it does to buy a dollar for delivery in two days.This is what is meant by a forward premium.We knew it was a premium because the forward rate is higher than the spot rate.If the forward rate had been lower than the spot rate we would have said that there was a forward discount concerning the amount of South Korean won that must be paid for the dollar 90 days forward.

We must take care when talking about discounts and premiums on forward foreign exchange contracts.Because buying one currency is the same as selling the other, there can be some ambiguity about which currency is being sold at a discount or premium.For example, some people would say that a 5.96% premium for the 90-day forward dollar is the same as a 5.96% discount for the 90-day forward won.We can work through an example to see how discounts and premiums are often presented in the financial press.

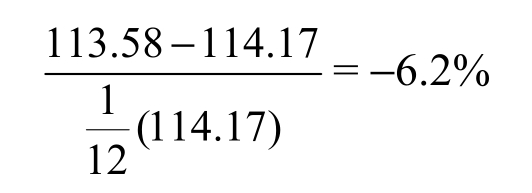

In the column labeled “Closing mid-point” we can see the Japanese yen is quoted spot as 114.170.This rate was calculated by using the bid/offer spread to calculate the bid/ask rate: 114.140-114.200.Taking the sum of the bid and the ask and dividing by two give the closing mid-point.In the column labeled “one month” we see that the mid-point rate for a one-month forward contract is 113.58.We know that the US dollar is at a discount to the yen because the dollar buys fewer yen for delivery in one month than it does for spot delivery.The last column labeled “% p.a.” we see in the table 6.1, means that the premium on the yen vis-à-vis the dollar is 6.2%, calculated by using the average forward and spot rates in Equation (6.2)to calculate the discount on the dollar:

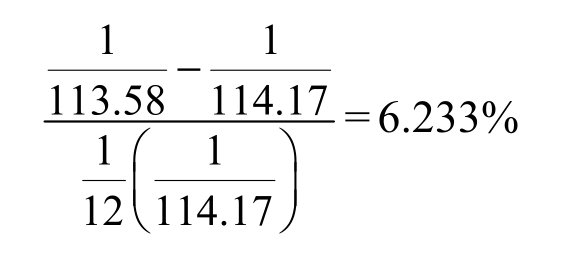

Because the discount on the dollar is approximately equal to the premium on the yen, it is reported as the premium on the yen.In fact, the premium on the yen is higher than 6.2%.Taking the reciprocals of S0(JPY/UD)and F0,1/12(JPY/USD)to get the (USD/JPY)rates gives a premium on the yen of

This having been said, in order to reduce the opportunities for confusion, we will always speak of the discount or premium in terms of the currency that is in the denominator of the exchange rate.Thus, if we give the CHF/USD exchange rate, we will speak of the discount or premium on the dollar or say the dollar is at a forward discount or premium.If it takes more Swiss francs to buy a dollar forward than it does to buy a dollar spot, we will say that there is a premium on the dollar or the dollar is at a premium.If it takes fewer Swiss francs to buy one dollar forward, we will say that there is a discount on the dollar or the dollar is at a discount.

● Conventions in forward quotations

There are basically two methods of expressing forward exchange rates.The first method is to quote the rate “outright” and is similar to spot quotes.It involves giving the number of units of one currency that it takes to buy one unit of another currency for delivery in the future.The second method presents the forward rate as a discount or premium on the spot rate and is called the swap rate.

When forward rates are quoted as a swap instead of outright, the spot rate is given and then the forward rate is given as a number of points that must be added or subtracted from the spot rate.Consider, for example, the rates set out in Table 6.2.On the USD/GBP rates, the bid points are larger than the ask points (80>78 and 213>210).This tells us that the pound is selling at a discount and that to obtain the outright forward rate we must subtract the bid-ask points from the spot rate.The reasons for this are simple.First of all, the spread on the forward rate should increase as the maturity of the contract increases.This is so partly because longer maturities are riskier than shorter maturities.To the extent that banks do not offset all their forward positions, they will demand a larger spread.The market also thins out as maturities increase, which makes it more difficult for banks that have contracted at a given rate to take an offsetting position.To compensate for this risk they will also require a larger spread.Secondly, the bid price must always be lower than the ask price.Hence, when bid points are higher than ask points, the only way to ensure that spreads will increase with maturity and that the bid price will always be lower than the ask price is to subtract.Table 6.3 shows the outright quotes for the USD/GBP exchange rate.Notice that the spread increases with the maturity of the forward contract.

Table 6.2 Example spot and forward rates

Table 6.3 Bid-ask rates, USD/GBP

Forward cross rate

Forward cross rates can be calculated in the same way as spot cross rates.Using the information in these tables, we can calculate the three-month CAD/GBP rate.First we have to get the GBP/USD rate.Remember that [GBP/USDbid] is equal to the reciprocal of [USD/ GBPask] and that[GBP/USDask] is equal to the reciprocal of [USD/GBPbid].Thus:

Three-month GBP/USD: 0.6055-0.6060

The three-month CAD/GBP cross bid rate can be obtained by selling pounds for dollars three months forward and paying GBP 0.6060, while simultaneously selling dollars three months forward and receiving CAD 1.1518.The bid rate will then be 1.1518/0.6060 = CAD 1.9007.Similarly, the three-month cross ask rate can be obtained by selling Canadian dollars for US dollars three months forward and paying CAD 1.1533 per US dollar, while simultaneously selling the US dollars three months forward and receiving GBP 0.6055 per dollar.The ask rate will then be 1.1533/0.6055 = CAD 1.9047.

While it is possible to calculate forward exchange rates in the foregoing manner, in practice there is a much easier method based on the interest rate parity hypothesis.We will look at this method in detail later in the chapter.

Reasons for using forward contracts

Regular quotes on forward contracts are limited to a relatively small number of currencies.The Euro, the Japanese yen and the British pound make up a large part of the whole market, although the Swiss franc and the Canadian dollar also account for considerable volume.Much of the activity comes from banks offsetting positions that they have taken in other transactions.As we mentioned, banks tend to trade on even multiples of 30 days such as one month, two months, three months, etc.However, when dealing with customers, banks stand ready to organize forward contracts for any period from three days to several years.

Another source of activity is from interest rate parity arbitraging if the forward premium of discount is out of line with the interest rate differential.

A common use of forward contracts is to eliminate uncertainty in commercial contracts arising from possible changes in the exchange rate.For example, an exporter who bills in foreign currency needs to know how many units of domestic currency he will receive for his goods.There is often a long lag between the time the sale is made and when the merchandise is delivered and paid for.In men’s and women’s apparel, for example, orders are placed six to nine months before delivery of the merchandise and payment is often made two to three months after delivery.A lot can happen in six months to a year so many firms take on a forward position to lock in their income in domestic currency.

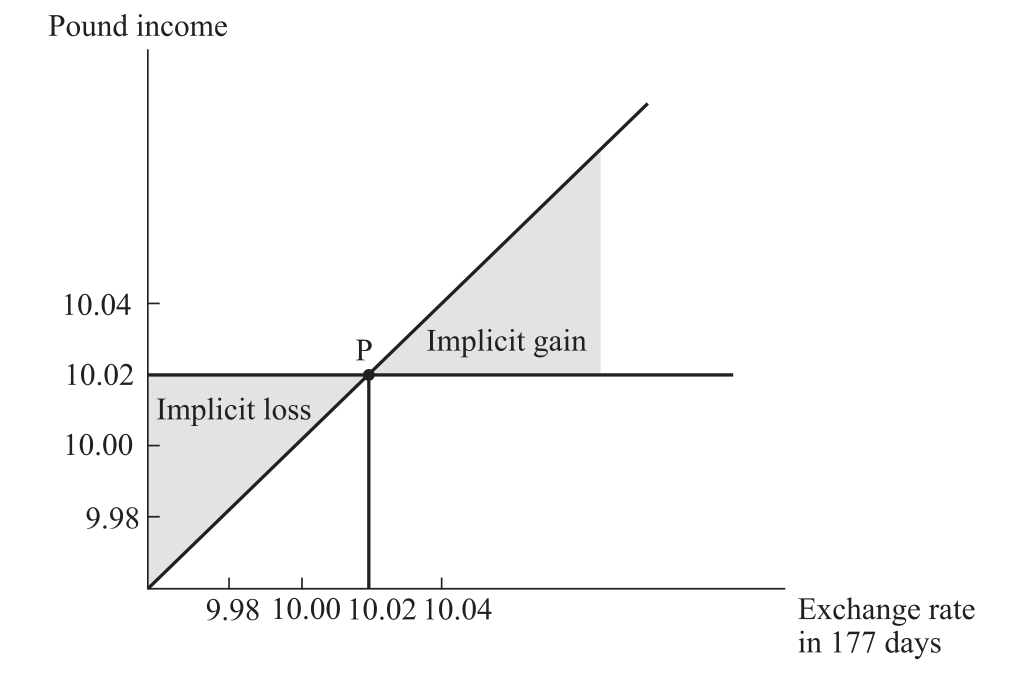

Suppose that on 1 September, 1998, Simay Ltd., a producer of stylish sportswear, takes an order for jogging suits to be delivered to its Danish client on 25 February of the following year.The order is for DKK 1,000,000 to be paid on delivery.The current exchange rate between the krone and the pound is DKK 10 = GBP 1.If the rate is the same on 25 February, Simay will receive GBP 100,000.If it goes to DKK 9.85 Simay will receive GBP 101,522.84, but if it falls to DKK 10.15 Simay will only receive GBP 98,522.17.The 177-day forward rate is DKK 10.02 and Simay decides to sell the DKK 1,000,000 forward and be sure to receive GBP 99,800.40.No matter what happens to the exchange rate Simay’s position remains the same.If, on 25 February, the exchange rate is DKK 10.02, Simay neither gains nor loses from the forward transaction.If the exchange rate is higher than 10.02, Simay avoids a loss.The shaded area to the right of point P represents the implicit gain associated with avoiding the loss.On the other hand, if the exchange rate is below 10.02, Simay forfeits a potential gain.The shaded area to the left of point P represents the implicit loss associated with the forfeited gain.

Figure 6.2 Forward cover for a commercial transaction

The same reasoning can be applied to investors who make forward contracts to lock in returns in domestic currency.Sometimes, however, forward transactions are undertaken to preserve the domestic currency value of an asset that will not be sold or cashed in over the life of the contract.

![]()

1.Costs on foreign exchange transactions are in the form of bid-ask spreads.They are generally very low on inter-bank transactions and higher on retail transactions depending on the size of the trade and the currencies traded.

2.The exchange rate of all currencies is given against the US dollar.The exchange rate between two currencies not involving the dollar is called the cross rate.Indicative cross rates can be calculated from the individual dollar exchange rates.Because of transaction costs, cross rates calculated in this way only indicate the range within which the cross rates must fall.

3.Forward exchange rates can be quoted in two ways.The first way is to quote the rate outright and is similar to spot quotes.It involves giving the number of units of one currency that it takes to buy one unit of another currency for delivery in the future.The second method presents the forward rate as a discount or premium on the spot rate and is called the swap rate.