Dollarization

Several countries have suffered currency devaluation for many years, primarily as a result of inflation, and have taken steps toward dollarization.Dollarization is the use of the US dollar as the official currency of the country.Panama has used the dollar as its official currency since 1907.Ecuador, after suffering a severe banking and inflationary crisis in 1998 and 1999, adopted the US dollar as its official currency in January 2000.One of the primary attributes of dollarization was summarized well by BusinessWeek in a December 11, 2000, article entitled “The Dollar Club”:

One attraction of dollarization is that sound monetary and exchange-rate policies no longer depend on the intelligence and discipline of domestic policymakers.Their monetary policy becomes essentially the one followed by the US and the exchange rate is fixed forever.

The arguments for dollarization follow logically from the previous discussion of the impossible trinity.A country that dollarizes removes any currency volatility (against the dollar)and would theoretically eliminate the possibility of future currency crises.Additional benefits are expectations of greater economic integration with the United States and other dollar-based markets, both product and financial.This last point has led many to argue in favor of regional dollarization, in which several countries that are highly economically integrated may benefit significantly from dollarizing together.

Three major arguments exist against dollarization.The first is the loss of sovereignty over monetary policy.This is, however, the point of dollarization.Second, the country loses the power of seignorage, the ability to profit from its ability to print its own money.Third, the central bank of the country, because it no longer has the ability to create money within its economic and financial system, can no longer serve the role of lender of last resort.This role carries with it the ability to provide liquidity to save financial institutions that maybe on the brink of failure during times of financial crisis.

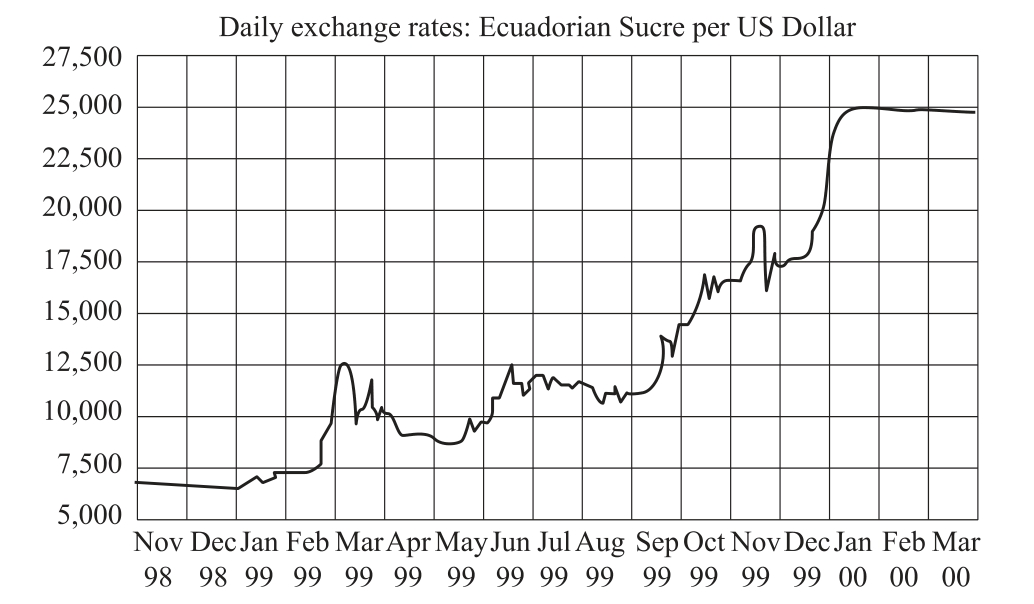

Ecuador.Ecuador officially completed the replacement of the Ecuadorian sucre with the US dollar as legal tender on September 9, 2000.This step made Ecuador the largest national adopter of the US dollar, and in many ways set it up as a test case of dollarization for other emerging market countries to watch closely.As shown in Figure 9.4, this was the last stage of a massive depreciation of the sucre in a brief two-year period.

Figure 9.4 The Ecuadorian Sucre exchange rate, November 1998-March 2000

Source: Pacific Currency Exchange, http://pacific.commerce.ubc.ca/xr 2001 by Prof.Werncer Antweiler.University of British Columbia, Vancouver, BC, Canada.

During 1999, Ecuador suffered a rising rate of inflation and a falling level of economic output.In March 1999, the Ecuadorian banking sector was hit with a series of devastating “bank runs,” financial panics in which all depositors attempted to withdraw all of their funds simultaneously.Although there were severe problems in the Ecuadorian banking system, the truth was that even the healthiest financial institution would fail under the strain of this financial drain.Ecuador’s president at that time, Jamil Mahuad, immediately froze all deposits (what was termed a bank holiday in the United States in the 1930s, in which banks closed their doors).The Ecuadorian sucre, which in January 1999 was trading at roughly Sucre 7,400/dollar, plummeted in early March to Sucre 12,500/dollar.Ecuador defaulted on more than $13.6 billion in foreign debt in 1999 alone.President Mahuad moved quickly to propose dollarization to save the failing Ecuadorian economy.

By January 2000, when the next president took office (after a rather complicated military coup and subsequent withdrawal), the sucre had fallen in value to Sucre25,000/dollar.The new president, Gustavo Naboa, continued the dollarization initiative.Although unsupported by the US government and the IMF, Ecuador completed its replacement of its own currency with the dollar over the next nine months.

The results of dollarization in Ecuador are still unknown.Ecuadorian residents immediately returned over $600 million into the banking system, money that they had withheld from the banks in fear of bank failure.This added capital infusion, along with new IMF loans and economic restructurings, allowed the country to actually close 2000 with a small economic gain of 1%.Inflation, however, remained high, closing the year at over 91% (up from 66% in 1999).Clearly, dollarization alone did not eliminate inflationary forces.Ecuador continues to struggle to find both economic and political balance with its new currency regime.

There is no doubt that for many emerging markets, a currency board, dollarization, and free-floating exchange rate regimes are all extremes.In fact, many experts feel that the global financial marketplace will drive more and more emerging market nations toward one of these extremes.There is a distinct lack of middle ground between rigidly fixed and free-floating extremes.In anecdotal support of this argument, a poll of the general population in Mexico in 1999 indicated that 9 out of 10 people would prefer dollarization over a floating-rate peso.Clearly, there are many in the emerging markets of the world who have little faith in their leadership and institutions to implement an effective exchange rate policy.