The principle of effective market classification

While Tinbergen’s instruments-targets rule shows us that we generally need two instruments to achieve both internal and external balance, it does not tell us which instrument should be assigned to which target.We have seen that we can use combinations of fiscal and monetary policy to achieve internal and external balance under fixed exchange rates, or we can use combinations of monetary of fiscal policy under floating exchange rates.

Mundell (1968)suggested that what he called the principle of effective market classification should be used by economic policy-makers in conjunction with Tinbergen’s instruments-targets rule.Mundell’s principle stated that “Policies should be paired with the objectives on which they have the most influence”.For instance, if monetary policy is the most effective instrument at controlling external balance, and fiscal policy is best at influencing output, then this is also the appropriate pairing of instruments to targets.The principle of effective market classification seems eminently sensible—by analogy a conductor should be assigned to conducting an orchestra and a doctor assigned to a hospital and not vice versa! What makes the Mundell principle of effective market classification interesting is the suggestion that if this principle is not adopted economies may suffer from cyclical instability.

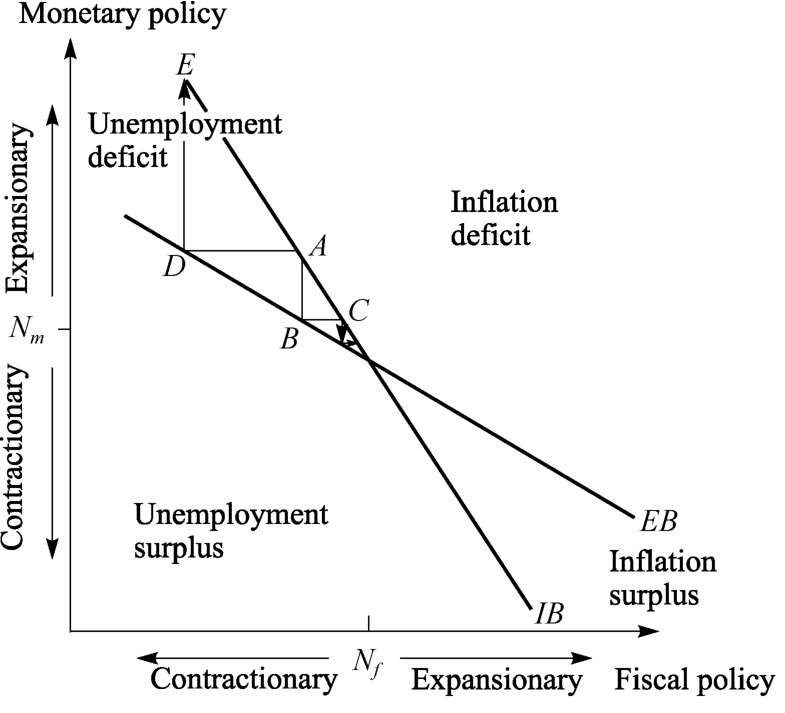

The problem for economic policy-makers to determine which instruments to assign to which targets, is termed the “assignment problem”.Mundell suggested that under fixed exchange rates, monetary policy should be assigned to external balance and fiscal policy to internal balance.An illustration of the assignment problem is shown in Figure 3.10 which illustrates internal and external balance schedules for various fiscal and monetary policy stances under a fixed exchange-rate regime.On the vertical axis monetary policy is neutral at point Nm but expansionary above this, while it is contractible below.Similarly, the fiscal policy stance is neutral at point Nf and expansionary to the right and contractible to the left.The internal balance schedule has a negative slope; this is because if we start at full employment a contractible monetary policy has to be accompanied by an expansionary fiscal to maintain full employment.To the right of the IB schedule the fiscal/monetary policy mix is so expansionary as to cause inflation, whereas to the left the fiscal/monetary policy mix is deflationary.

Figure 3.10 The assignment problem

The external balance schedule may have a positive or negative slope; this is because an expansionary fiscal policy has two conflicting effects on the balance of payments as we saw in Figure 3.6 and Figure 3.7.On the one hand, the increase in income leads to a deterioration in the current account which worsens the balance of payments, but on the other the rise in interest rates leads to an inflow of capital which improves the balance of payments.In Figure 3.10 we have drawn the EB schedule with a negative slope meaning that an expansionary fiscal policy causes a net deterioration in the balance of payments (the current account effect dominates the capital account effect).This being the case, when fiscal policy is expansionary monetary policy has to be contractible, which by raising the domestic interest rate increases capital inflows to ensure equilibrium in the balance of payments.

The IB schedule is drawn steeper than the EB schedule; this must be the case because a fiscal expansion which causes a rise in income of x percent will cause less of a deterioration in the balance of payments than a monetary policy that increases income by the same amount.This is because a fiscal expansion will lead to a rise in interest rates which leads to partially offsetting capital inflows, while a money expansion leads to a fall in interest rates leading to an additional deterioration in the balance of payments above the income effect.Hence, monetary policy has more effect on external balance than fiscal policy.As monetary policy is relatively more effective at influencing external balance, then fiscal policy is relatively more effective with respect to internal balance.

According to Mundell’s classification, if we are at point A with internal balance but a balance-of-payments deficit a contractible monetary policy moves the economy to, say, point B on the external balance curve, but this leads to unemployment which is then tackled by an expansionary fiscal policy moving to point C on the internal balance curve.This pushes the balance of payments back into deficit and is then accompanied by a monetary contraction to achieve external balance.Each time we need less and less adjustment of monetary and fiscal policy.We have a stable assignment as we are clearly converging to the intersection of the internal and external balance schedules.

Suppose policy-makers get the assignment wrong and use fiscal policy to eradicate the balance-of-payments deficit, and monetary policy for internal balance.In such circumstances the fiscal contraction moves the economy from point A to point D, and external balance is achieved but at the cost of high unemployment.If the authorities then use an expansionary monetary policy to achieve internal balance the economy moves from point D to point E.Clearly, such a policy assignment proves to be unstable, moving the economy away from the simultaneous achievement of internal and external balance the danger exists that the authorities could get the assignment wrong and cause considerable damage to the economy before they eventually reverse their assignment to the correct one.Given this, it may be wise to try to achieve targets gradually by adjustment policy instruments slowly to make sure they are having the intended effect.

Unfortunately there is no unambiguous answer to the assignment problem.Consider, for example, our analysis of a small open economy under conditions of perfect capital mobility.We have seen that the effectiveness of fiscal and monetary policy at influencing output depends upon whether or not there is a fixed or floating exchange rate.If the exchange rate is fixed then fiscal policy should be paired with the objective of full employment, whereas if the exchange rate is floating then monetary policy should be assigned.The assignment problem has no simple solution and is considerably more complicated once we have three targets depending upon the structural parameters governing the behavior of an economy.This includes amongst others, the degree of capital mobility; marginal propensity to save and import; income and interest elasticity of demand for money; the price elasticity of demand for imports and exports; and responsiveness of investment to interest rate variations.