2.3 The monetary approach to the balance of paymen...

The balance of payments is essentially a monetary phenomenon.Not only is the balance of payments a measurement of monetary flows, but such flows can only be explained by disequilibrium in the stock, demand for and supply of money.

There are three key assumptions that underlie the monetary model.They are a stable money demand function, a vertical aggregate schedule and purchasing power parity (PPP).The simple monetary model invokes the three assumptions and then proceeds with the use of some accounting identities and behavioral assumptions to develop a theory of the balance of payments.

The domestic monetary supply in the economy is made up of two components:

Here Ms stands for the domestic money base, D for the domestic bond holdings of the monetary authorities, and R for the reserves of foreign currencies valued in the domestic currency.

Equation (2.6)says that the domestic money base is made up of two components.This monetary base can come into circulation in one of two ways:

1.The authorities may conduct an open market operation (OMO), which is a purchase of treasury bonds held by private agents by the central bank.This increases the central bank’s monetary liabilities and increases its assets of domestic bond holdings which are the domestic component of the monetary base as represented by D.

2.The authorities may conduct a foreign exchange operation (FXO), which is a purchase of foreign currency assets (money or foreign treasury bonds)held by private agents by the central bank.This again increases the central bank’s monetary liabilities and also increases its assets of foreign currency and foreign bonds which are represented by R.

We can now rewrite equation (2.6)in a different form as:

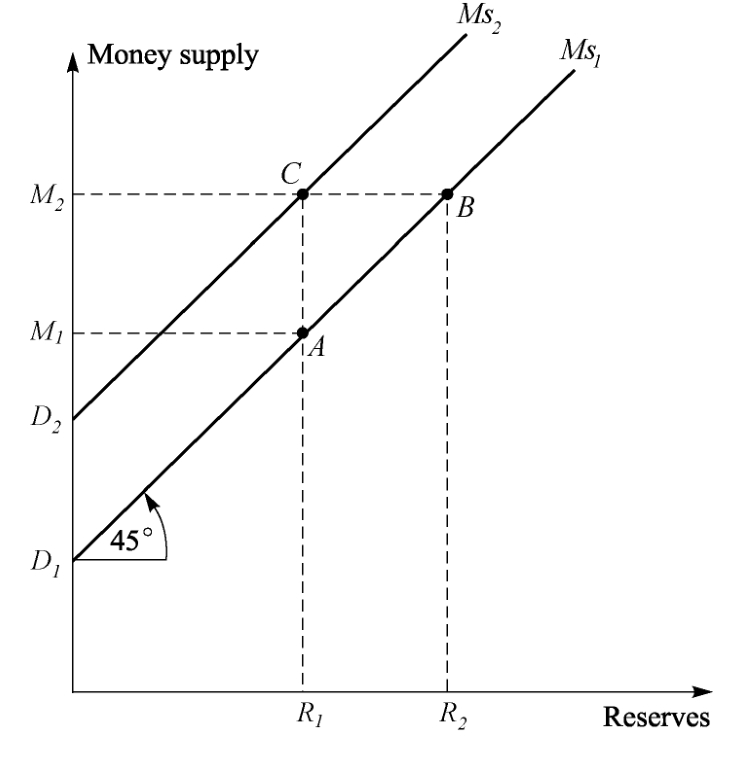

Which states that any increase (decrease)in the domestic money supply can come about through either an OMO as represented by dD or a FXO as represented by dR.The relationship between the money supply and reserves is depicted in Figure 2.2.

In Figure 2.2 at point D1 all the domestic money supply is made up entirely of the domestic component since reserves are zero.For convenience we set the exchange rate of domestic to foreign currency equal to unity; this being the case an increase of 1 unit of foreign currency leads to an increase in the domestic money supply of 1 unit, so that when reserves are R1 the money supply is M1, that is, D1+R1.

Figure 2.2 The money supply and reserves

An OMO will have the effect of shifting the Ms schedule by the amount of the increase in the central bank’s domestic bond holdings.An OMO which increases the domestic component of the monetary base from D1 to D2 shifts the money supply schedule from Ms1 to Ms2, and the total money supply rises from M1 to M2.By contrast, an expansion of the money supply due to a purchase of foreign currencies, that is an FXO, increases the country’s foreign exchange reserves from R1 to R2.This too has the effect of raising the money stock from M1 to M2 and is represented by a movement along the money supply schedule Ms1 from point A to point B.

The monetarists view balance-of-payments surplus and deficit as monetary flows due to stock disequilibrium in the money market.A deficit in the balance of payments is due to an excess of the stock of money in relation to money demand, while a surplus is a monetary flow resulting from an excess demand for money in relation to the stock money supply.Thus a balance-of-payments disequilibrium is merely a reflection of a disequilibrium in the money market.In this sense the monetary flows are the “autonomous” items in the balance of payments, while the purchases and sales of goods/services and investments (long, medium and short-term)are viewed as the “accommodating” items.This is completely the reverse of the Keynesian approach which views the current account items as the autonomous items and capital account and reserve changes as the accommodating items.This different way of looking at the balance-of-payments statistics is something contrasted by saying that Keynesians look at the statistics from the “top down” (that is, the change in reserves).

Monetarists observe that the overall balance of payments consists of the current account balance, the capital account balance, and change in the authorities’ reserves.That is:

So that:

Here CA stands for the current account balance, K for the capital account balance, and dR for the change in the authorities’ reserves.

If the recorded dR in the balance-of-payments accounts is positive, this means that the combined current account and capital accounts are in deficit.This implies that reserves have fallen as the authorities have purchased the home currency with foreign currency reserves.

Equation (2.8)is a distinct way of viewing the balance of payments; increases in reserves due to purchases of foreign currencies constitute a surplus in the balance-of-payments, while falls in reserves resulting from purchases of the domestic currency represent a deficit in the balance of payments.If the authorities do not intervene in the foreign exchange market, that is the currency is left to float, then reserves do not change and as far as the monetary view is concerned the balance of payments is in equilibrium.Under a floating exchange-rate regime a current account deficit must be financed by an equivalent capital inflow so the balance of payments is in equilibrium.

The monetary approach provides a distinctive and clear analysis of the effects of a devaluation and monetary expansion on the balance of payments.Its emphasis on disequilibrium in the balance of payments being a flow response to stock disequilibrium in the money market represents an important contribution to the research on international economics.

Another significant contribution of the monetary approach is that it provides a rich set of policy recommendations.A country that opts to fix its exchange rate will lose its monetary autonomy, and a monetary expansion can lead to temporary balance-of-payments deficits.Whereas a country that allows its currency to float will have monetary autonomy but a monetary expansion then leads to a depreciation of its currency.Hence, it provides a warning to policy-makers that reckless monetary expansion can lead to balance-of-payments problems under fixed exchange rates, or a currency problem under floating exchange rates.

With regard to the effects of a devaluation of a currency, starting from a position of equilibrium, the monetary approach suggests that there will be an unambiguous transitory surplus in the balance of payments.This stands in contrast to the elasticity and absorption approaches, which suggest the effects are ambiguous.It must be borne in mind, however, that the monetary model is referring to the combined current and capital account whereas the latter two are concerned exclusively with the current account.Finally it needs to be remembered that the monetary approach does not specify precisely how temporary the resulting surplus is; presumably this varies on a country-by-country basis.

![]()

1.Only if the sum of the foreign elasticity of demand for exports and the home country elasticity of demand for imports is greater than unity, that is y1+y2>1, a devaluation will improve the current account.If the sum of the elasticity is less than unity then devaluation will lead to a deterioration of the current account.This is known as the Marshall-Lerner condition.

2.A general consensus accepted by most economists is that elasticity is lower in the short run than in the long run, in which case the Marshall-Lerner conditions may only hold in the medium to long run.This possibility leads to the phenomenon of what is popularly known as the J-curve effect.

3.The current account (CA)represents the difference between domestic output and domestic absorption.A current account surplus means that domestic output exceeds domestic spending, while a current account deficit means that domestic output is less than domestic spending.

4.The monetarists view balance-of-payments surplus and deficit as monetary flows due to stock disequilibrium in the money market.A deficit in the balance of payments is due to an excess of the stock of money in relation to money demand, while a surplus is a monetary flow resulting from an excess demand for money in relation to the stock money supply.Thus a balance-of-payments disequilibrium is merely a reflection of disequilibrium in the money market.