A small open economy with perfect capital mobility

One prominent feature of the post-Second World War international monetary system has been the increasing integration of international capital markets.There has been a great deal of discussion about the desirability of these capital flows and how they might threaten the ability of authorities to conduct effective economic policies.In classic papers, Mundell (1962)and Fleming (1962)sought to examine the implications of high capital mobility for a small country that had no ability to influence world interest rates.Their papers showed that for such a country, the choice of exchange-rate regime would have a radical implication, concerning the effectiveness of monetary and fiscal policy in influencing the level of economic activity.

The model assumes a small country facing perfect capital mobility.Any attempt to raise the domestic interest rate leads to a massive capital inflow to purchase domestic bonds pushing up the price of bonds until the interest rate returns to the world interest rate.Conversely, any attempt to lower the domestic interest rate leads to a massive capital outflow as international investors seek higher world interest rates.Such massive bonds sales mean that bond prices fall and the domestic interest rate immediately returns to the world interest rate so as to stop the capital outflow.The implication of perfect capital mobility is that the BP schedule for a small open economy becomes a horizontal straight line at a domestic interest rate that is the same as the world interest rate.

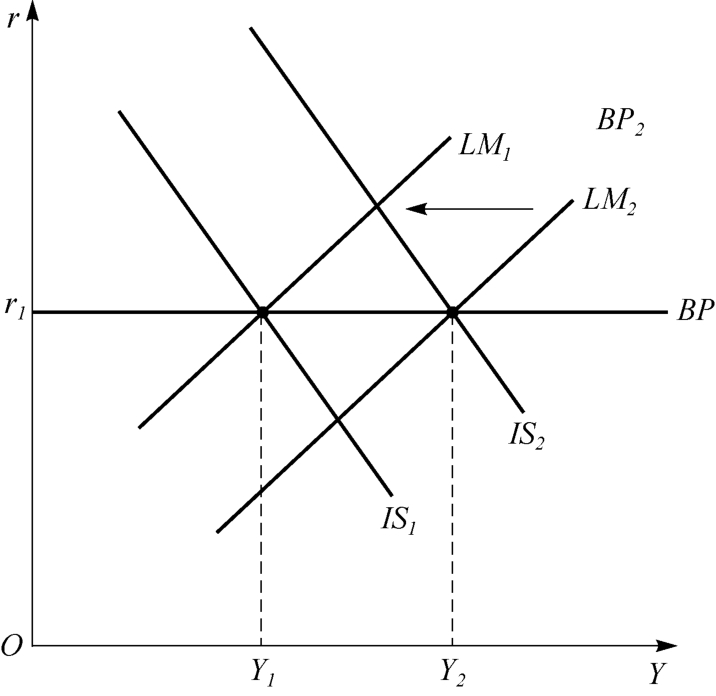

Figure 3.8 depicts a small open economy with a fixed exchange rate.The initial level of income is where the IS-LM curves intersect at the income level Y1 which is below the full employment level of income Yf.If the authorities attempt to raise output by a monetary expansion, the LM schedule shifts to the right from LM1 to LM2; there is downward pressure on the domestic interest rate and this results in a massive capital outflow.This capital outflow means that there is pressure for a devaluation of the currency, and the authorities have to intervene in the foreign exchange market to purchase the home currency with reserves.Such purchases result in a reduction of the money supply in the hands of private agents, and the purchases have to continue until the LM curve shifts back to its original position at LM1 where the domestic interest rate is restored to the world interest rate.With perfect capital mobility, any attempt to pursue a sterilization policy leads to such large reserve losses that it cannot be pursued.Hence, with perfect capital mobility and fixed exchange rates, monetary policy is ineffective at influencing output.

Figure 3.8 Fixed exchange rates and perfect capital mobility

By contrast, if there is a fiscal expansion this shifts the IS schedule to the right from IS1 to IS2, and this puts upward pressure on the domestic interest rate and leads to a capital inflow.To prevent an appreciation the authorities have to purchase the foreign currency with domestic currency.

This means that the amount of domestic currency held by private agents increases and the LM1 schedule shifts to the right.The increase in the money stock continues until the LM schedule passes through the IS2 schedule at the initial interest rate.Hence, under fixed exchanged rates and perfect capital mobility an active fiscal policy alone has the ability to achieve both internal and external balance.This is an exception to the instruments-targets rule, although monetary policy does have to passively adjust to maintain the fixed exchange rate.

Floating exchange rates and perfect capital mobility

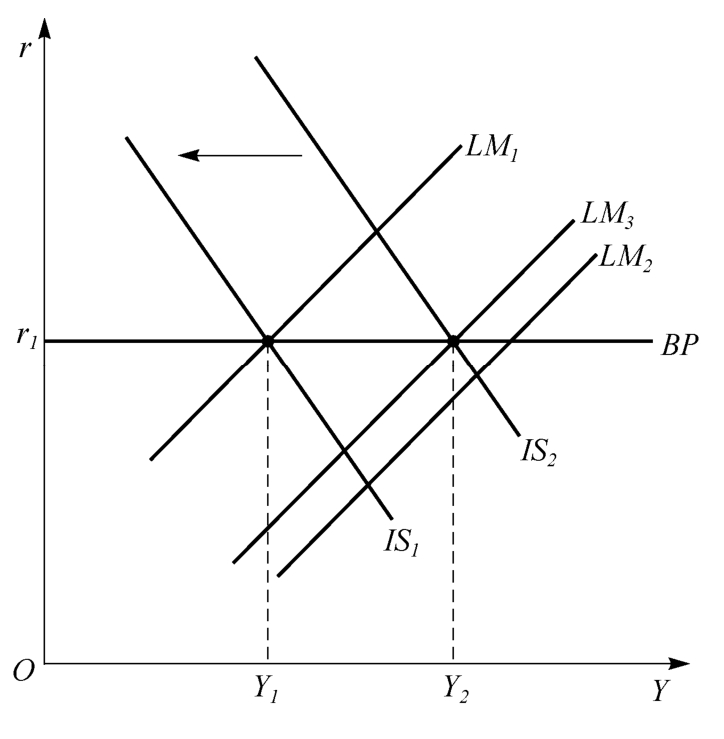

In Figure 3.9 initial equilibrium is at the income level Y1 where the IS1 schedule intersects the LM1 schedule.In this case we have a floating exchange rate.A monetary expansion shifts the LM schedule from LM1 to LM2 leading to downward pressure on the interest rate, a capital outflow, and a depreciation of the exchange rate.The depreciation leads to an increase in exports and reduction in imports so shifting the IS curve to the right and the LM schedule to the left, so that final equilibrium is obtained at a higher level of income say Y2.Clearly with an appropriate initial monetary expansion the authorities could obtain both internal and external balance by monetary policy alone.

Figure 3.9 Floating exchange rates and perfect capital mobility

Suppose, instead, the authorities attempt to expand output by an expansionary fiscal policy.The increased government expenditure shifts the IS schedule to the right from IS1 to IS2, but the bond sales that finance the expansion lead to upward pressure on the domestic interest rate resulting in a massive capital inflow and an appreciation of the exchange rate.The appreciation of the exchange rate results in reduction of exports and an increase in imports, and this forces the IS schedule back to its original position.Hence, with perfect capital mobility and a floating exchange rate, fiscal policy is ineffective at influencing output.

The result that fiscal policy is very effective at influencing output under fixed exchange rates and monetary policy is very effective under floating exchange rates with perfect capital mobility is of considerable relevance to economic policy design.Under fixed rates policy makers will pay more attention to fiscal policy than under floating rates when more emphasis will be placed on monetary policy.The degree of capital mobility and the exchange rate regime both demonstrate that appropriate economic policy design in an open economy is very different from that in a closed economy context.

The contrast between the effectiveness of fiscal and monetary policy with perfect capital mobility under different exchange-rate regimes is one of the most famous results in international economics.Monetary policy is ineffective at influencing output floating exchange rates.By contrast, fiscal policy alone is effective at influencing output under a fixed exchange rate, while it is ineffective under floating exchange rates.