Origins and development

The Eurocurrency market is not a new phenomenon.Before and after World War I banks in most European countries accepted deposits in many different currencies.The origin of today’s Eurocurrency market, however, is usually credited to countries of the former Soviet bloc who, during the height of the Cold War, feared that their dollar reserves might be frozen if held in the United States.This was the heyday of the gold exchange standard and the Soviet bloc countries were obliged to accept dollars if they wanted to do business with the West.To avoid having their dollar balances blocked by the Americans, they held them with banks located in England and France.

The threat of sanctions may have created the post-World War II Eurodollar market, but it was the reality of regulations that made it prosper.Two US Federal Reserve Board regulations—Regulation Q and Regulation M—were especially influential in the development of the Eurodollar market.Regulation Q set interest rate ceilings on deposits in the United States.European banks, of course, were not subject to this regulation and, consequently, could pay higher rates for dollar deposits than American banks.This made it attractive to deposit dollars in the European markets where the rates were higher.In fact, many US banks set up overseas branches to take these funds.

A major instrument of monetary policy is the reserve ratio that requires commercial banks to hold a proportion of their deposits in an account with the central bank.Regulation M established the reserve ratio requirement for the US banking system.Reserves pay no interest and, hence, represent a high cost for banks.Consider, for example, a situation where the reserve ratio is 5% and the interest rate on deposits is 10%.

If a bank receives a deposit of USD 1,000, it pays interest on the full USD 1,000.However it only has effective use of USD 950 because 5% of the deposit must be held without interest with the central bank.Thus, the total cost of the funds is 10.53%, the USD 100 of interest divided by USD 950, the amount that it can effectively use; European banks were under no obligation to maintain fractional reserves on dollar deposits.This lowered their costs relative to domestic banks and made it possible for them to pay higher rates of interest to attract deposits.

Two other regulations that contributed to the development of the Eurodollar market came about as a result of the failing gold exchange standard.The US monetary authorities refused to take the painful step of reining in the US money supply in order to save the gold exchange standard.Instead they tried regulations as a means of improving the capital account:

● To discourage non-residents from borrowing in the United States the interest equalization tax was passed in 1963.It was a tax on US residents’ earnings on foreign securities.To compensate for the tax, foreign borrowers were obliged to pay higher interest rates, which made it costly for foreign firms and governments to borrow in the United States.Many turned to the Eurodollar market where no such restrictions existed.

● To discourage US corporations from lending overseas restrictions were placed on non-domestic uses of domestically generated funds.The voluntary restrictions of 1965 on borrowing funds in the United States for reinvestment abroad became mandatory in 1968.Under these restrictions many US firms with plans for overseas projects simply shifted their financing requirements to the Eurodollar market.

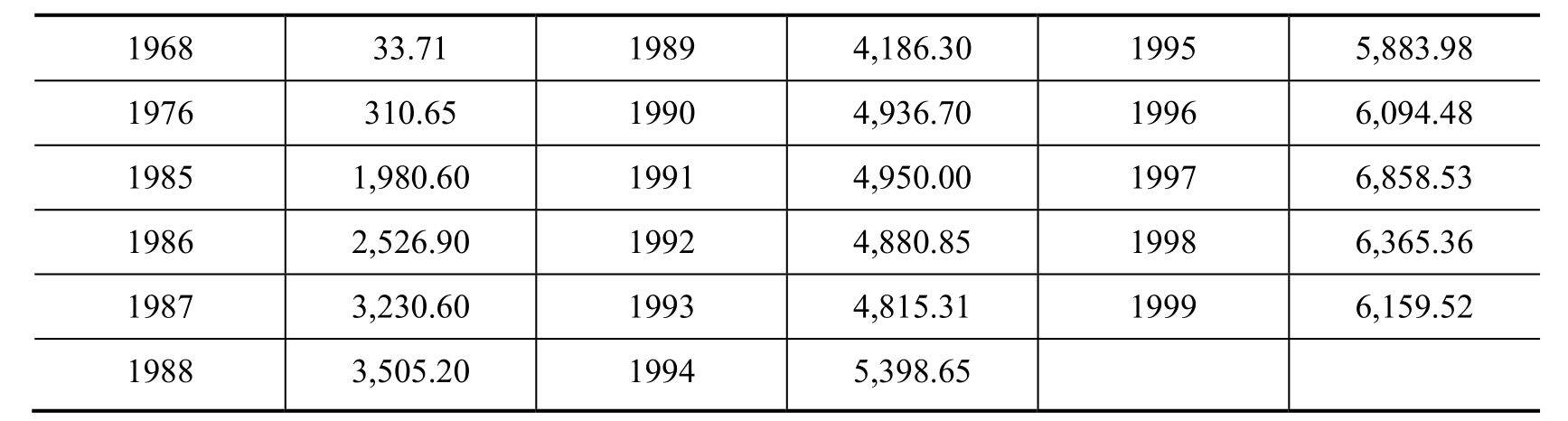

Special regulations were not the only reason for the development of the Eurocurrency market.By the mid-1970s Regulation Q was inoperative, the interest equalization tax was abolished and most restrictions on overseas investment had been lifted.Still, as we can see in Table 10.1, the Eurocurrency market continued to grow by leaps and bounds.Its nature is such that some cost savings are inherent.As a wholesale market dealing in large quantities, economies of scale can be achieved, which lower costs.Because the participants are also all professionals, costly regulatory supervision and consumer protection such as deposit insurance are unnecessary.Furthermore, Eurocurrency transactions are simply more convenient in today’s global economy.The development of cross-border commercial transactions has generated multiple currency cash flows that corporate treasurers are obliged to manage.It is impractical to deal with a different bank in a different country for each separate currency.Alternatively, dealing with one bank would also be costly and inefficient if it meant systematically converting all foreign currency cash flows into domestic currency when they arrive, only to reconvert into foreign currency when payments must be made.The Eurocurrency market makes it possible to deal with an easily accessible, well known bank that can handle all currency needs.

Thus, factors of cost and convenience are behind the emergence and growth of all the Eurocurrencies.Depositors want to receive the highest yield while borrowers want to pay the lowest cost, and the nature of the Euromarket and the absence of restrictions make it possible to fulfill these requirements.

Table 10.1 Size of the Eurocurrency market (bank liabilities in foreign currencies, USD bn), 1968-1999

Source: Bank for International Settlements