Achieving monetary unification

If the euro is to be a successful replacement of the currencies of the participating EU states, it must have a solid economic foundation.The primary driver of a currency’s value is its ability to maintain its purchasing power (money is worth what money can buy).The single largest threat to maintaining purchasing power is inflation.So, job one for the EU since the beginning has been to construct an economic system that would work to prevent inflationary forces from undermining the euro.

Fiscal policy and monetary policy.Monetary policy for the EMU is conducted by the ECB, which has one responsibility: to safeguard the stability of the euro.Following the basic structures that were used in the establishment of the Federal Reserve System in the United States and the Bundesbank in Germany; the ECB is free of political pressures that have historically caused monetary authorities to yield to employment pressures by inflating economies.The ECB’s independence allows it to focus simply on the stability of the currency without falling victim to this historical trap.

Fixing the value of the euro.The December 31, 1998, fixing of the rates of exchange between national currencies and the euro were permanent fixes for these currencies.The United Kingdom has been skeptical of increasing EU infringement on its sovereignty and has opted not to participate.Sweden, which has failed to see significant benefits from EU membership (although it is one of the newest members), has also been skeptical of EMU participation.Denmark, like the United Kingdom and Sweden, has a strong political element that is highly nationalistic and so far has opted not to participate.Norway has twice voted down membership in the EU and thus does not participate in the euro system.

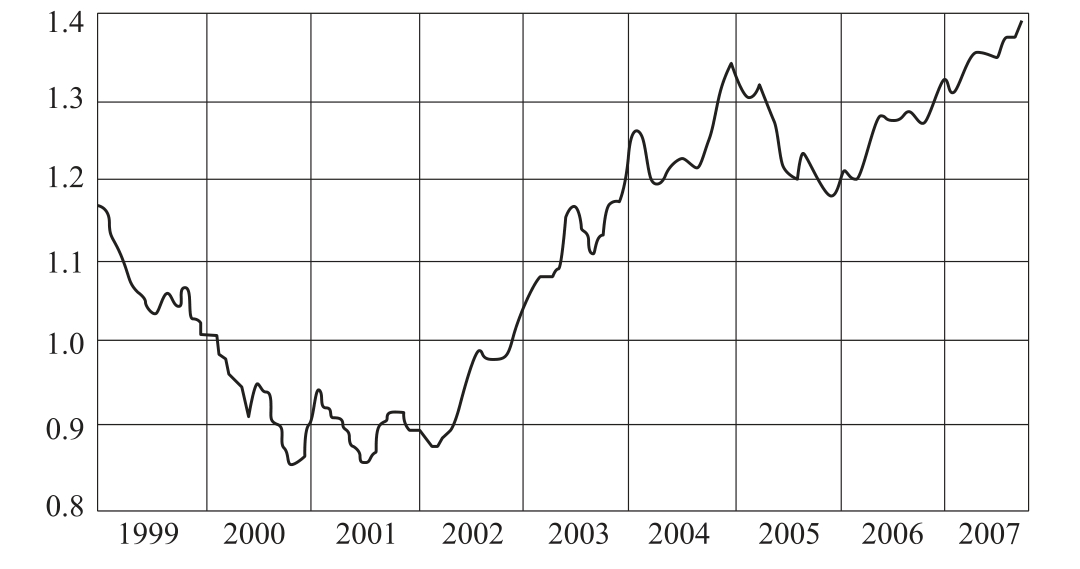

On January 4, 1999, the euro began trading on world currency markets.Its introduction was a smooth one.The euro’s value slid steadily following its introduction, however, primarily as a result of the robustness of the US economy and US dollar, and continuing sluggish economic sectors in the EMU countries.Figure 9.5 illustrates the euro’s value since its introduction in January 1999.After declining in value against the US dollar over 1999 and 2000, the euro traded in a relatively narrow band throughout 2001.Beginning in early 2002, however, the euro started a strong and steady rise in value versus the dollar, peaking at $1.50/€ in late 2007.

Figure 9.5 The US Dollar/Euro spot exchange rate, 1999-2007 (monthly average)

Note: Time period shown in diagran: 1/Jan/1999-27/Sep/2007.

Source: © 2007 by Prof.Werner Antweifer, University of British Columbia, Vancouver, BC, Canada.

Causes of the dollar decline.Since the introduction of the euro, the United States has experienced severe balance of payments deficits on the current account.The biggest bilateral deficits were with China and Japan.However, in order to protect their export competitiveness, both China and Japan followed macroeconomic policies that would maintain relatively fixed rates of exchange between their currencies and the US dollar.In order to accomplish this result, both China and Japan had to intervene in the foreign exchange market by buying massive amounts of US dollars while selling corresponding amounts of their own currencies, the Chinese yuan, and the Japanese yen.These purchases showed up as capital inflows into the United States.However, as the United States has continued to maintain historically low interest rates—both to stimulate the domestic economy and to promote liquidity in the financial system following the subprime mortgage failures in 2007—some critics wonder whether China and Japan will continue to hold such large quantities of US dollars.

Furthermore, several Asian and Middle Eastern governments are beginning to create so-called Sovereign Wealth Funds to use their accumulating US dollar balances.Sovereign Wealth Funds are government owned and funded investment funds that are either acquiring or taking a significant interest in private companies and major foreign banks in the United States and other Western countries.They are the subject of growing concern as foreign nations invest within other countries.

Expansion of the European Union and the euro.In January 2007, two more countries were added to the EU’s growing membership—Bulgaria and Romania.Their entry was little more than two years after the EU had added 10 more countries to its ranks.To date, only one of these 12 new members has actually adopted the euro.Although all members are expected eventually to replace their currencies with the euro, recent years have seen growing debates and continual postponements by the new members in moving toward full euro adoption.

The euro and growth.Prior to the introduction of the euro, opponents thought political and economic conditions were unfavorable for a common currency.Most of the countries that eventually adopted the euro, such as Germany, France, and Italy, lacked the flexible labor markets they would need to compensate for losing individual (country-level)control over monetary policy as a tool to promote growth.Since the individual members of the BU cannot devalue their currencies, they would need to rely mainly on coordinated fiscal policies to stimulate growth.It is probably impossible to conduct a centralized monetary policy that fits all member countries.Some members are growing and some are not.Unemployment has been fairly high in some members but lower in others.

Evaluating the euro.Apart from issues of growth and employment, the euro has had a mixed record of success and failure.As more and more dissimilar countries join the EU, it may prove more difficult for the benefits of euro adoption to win out.