3.1 The problem of internal and external balance

To appreciate the development of the postwar literature on open economies readers need to bear in mind that between 1948 and 1973 the international monetary system was one of fixed exchange rates, with the major currencies being pegged to the US dollar.Only in cases of “fundamental disequilibrium” were authorities allowed to devalue or revalue their currency.This meant that there was considerable interest in the relative effectiveness of fiscal and monetary policies as a means of influencing the economy.Although economic policy-makers generally have many macroeconomic aims, the discussion in the 1950s and 1960s was primarily concerned with two objectives.The principal goal was achieving full employment for the labor force along with a stable level of prices which may be termed internal balance.Although governments were generally committed to achieving full employment, it is widely recognized that expanding output in an open economy will have implications for the balance of payments.For instance, expanding output and employment will result in greater expenditure on imports and consequently will lead to a deterioration of the current account.As authorities had agreed to maintain fixed exchange rates, they were interested in running an equilibrium in the balance of payments; that is, balance in the supply and demand for their currency.This latter objective can be termed external balance.

Changes in fiscal and monetary policies which aim to influence the level of aggregate demand in the economy are termed expenditure changing policies.Whereas policies such as devaluation/revaluation of the exchange rate which attempt to influence the composition of spending between domestic and foreign goods are known as expenditure switching policies.

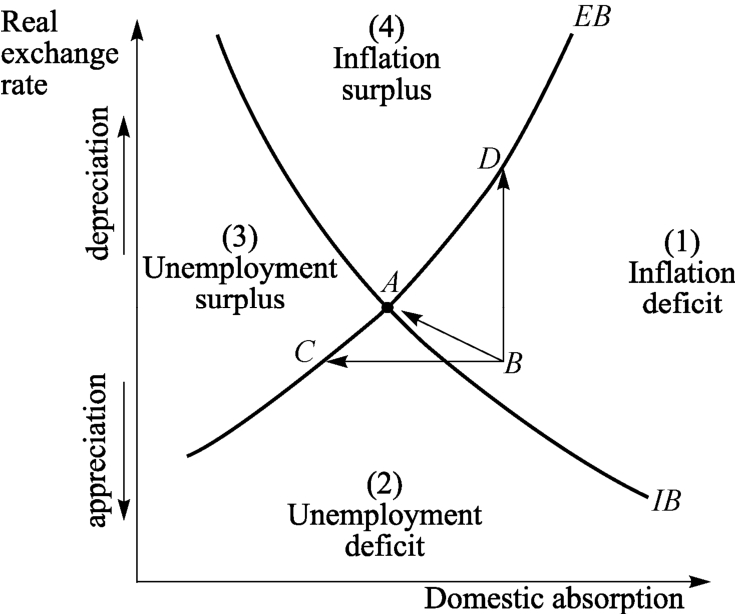

Much of the 1950s and 1960s literature was concerned with how the authorities might simultaneously achieve both internal and external balance.The policy problem of achieving both was conceptualized by Trevor Swan (1955)in what is known as the Swan diagram, which is depicted in Figure 3.1.On the vertical axis is the real exchange rate, defined as domestic currency units per unit of foreign currency so that a rise represents a real depreciation which implies improved international competitiveness.On the horizontal axis is the amount of real domestic absorption which represents the sum of consumption, investment and government expenditure.

Figure 3.1 The Swan diagram

The IB schedule represents combinations of the real exchange rate and domestic absorption for which the economy is in internal balance; that is, full employment with stable prices.The IB schedule is downward-sloping from left to right.This is because an appreciation (fall)of the real exchange rate will reduce exports and increase imports; therefore to maintain full employment it is necessary for there to be an increase in domestic expenditure.To the right of the IB schedule there are inflationary pressures in the economy because for a given exchange rate domestic expenditure is greater than that required to produce full employment; while to the left there are deflationary pressures because expenditure is short of that required to maintain full employment.

The EB schedule shows combinations of the real exchange rate and domestic absorption for which the economy is in external balance; that is, equilibrium in the current account.The EB schedule is upward-sloping from left to right.It is because a depreciation of the exchange rate will increase exports and reduce imports, so to prevent the current account moving into surplus requires increased domestic expenditure to induce an offsetting increase in imports.To the right of the EB schedule domestic expenditure is greater than that required for current account equilibrium, so the result is a current account deficit, while to the left there is a current account surplus.

Hence, the Swan diagram is divided into four zones depicting different possible states for an economy:

Zone 1—a deficit and inflationary pressures.

Zone 2—a deficit and deflationary pressures.

Zone 3—a surplus and deflationary pressures.

Zone 4—a surplus and inflationary pressures.

Only at point A where the IB and EB schedules intersect is the economy in both internal and external equilibrium.Suppose that the economy for some reason finds itself at point B in zone 1, experiencing both inflationary pressures and a current account deficit.If the authorities maintain a fixed exchange rate and try to reduce the current account deficit by cutting back real domestic expenditure they move the economy towards point C; achieving external balance by using expenditure-reducing policies alone would require such a cut back in absorption that the economy is pushed into recession, resulting in unemployment.Alternatively, the authorities might try to tackle the deficit by devaluing the exchange rate; this has the effect of moving the economy towards point D on the EB schedule.While the devaluation has the effect of reducing the current account deficit it dose so at the expense of adding further inflationary pressures to the economy.This is shown by the fact that the economy moves further away from the internal balance schedule.

A major lesson of this simple model is that the use of one instrument, be it fiscal expansion or devaluation to achieve two targets—internal and external balance, is most unlikely to be successful.To move from point B to point A, the authorities need to both deflate the economy and undertake a devaluation by appropriate amount.The deflation will control inflation and the devaluation improve the current account so that the two objectives can be met.The idea that a country generally requires instruments as many as it has targets was elaborated by the Nobel Prize-winning Dutch economist Jan Tinbergen (1952), and is popularly known as Tinbergen’s instruments-targets rule.

While the Swan diagram provides a useful conceptual framework for economic policy discussion it is rather simplistic in that the underlying economic relationships are not explicitly defined.Furthermore, there is no role for international capital movements that were an increasingly important feature of the post-Second World War international economy.In addition there is no distinction made between monetary and fiscal policies as means of influencing aggregate demand and output in the economy.