2.1 The elasticity approach to the balance of paym...

This approach provides an analysis of what happens to the current account balance when a country devalues its currency.The analysis was pioneered by Alfred Marshall, Abba Lerner and later extended by Joan Robinson (1937)and Fritz Machlup (1955).At the outset, the model makes some simplified assumptions: it focuses on demand conditions and assumes that the supply elasticity for the domestic export goods and foreign import goods are perfectly elastic, so that changes in demand volumes have no effect on prices.In effect, these assumptions mean that domestic and foreign prices are fixed so that changes in relative prices are caused by changes in the nominal exchange rate.

The central message of the elasticity approach is that there are two direct effects of a devaluation on the current balance, one of which works to reduce a deficit whilst the other actually contributes to making the deficit worse than before.Let us consider these two effects in some detail.

We introduce two definitions: the price elasticity of demand for exports y1, is defined as the percentage change in exports over the percentage change in price as represented by the percentage change in the exchange rate.And the price elasticity of demand for imports y2 is defined as the percentage change in imports over the percentage change in their price as represented by the percentage change in the exchange rate.Only if the sum of the foreign elasticity of demand for exports and the home country elasticity of demand for imports is greater than unity, that is y1+y2>1, a devaluation will improve the current account.If the sum of these two elasticity is less than unity then a devaluation will lead to a deterioration of the current account.This is known as the Marshall-Lerner condition.

There are three possible scenarios following a devaluation, and two effects in play once a currency is devalued:

1.The price effect—exports become cheaper measured in foreign currency.Imports become more expensive measured in the home currency.

2.The volume effect—the fact that exports become cheaper should encourage an increased volume of exports, and the fact that imports become more expensive should lead to a decreased volume of imports.The volume effect clearly contributes to improving the current account.

The net effect depends upon whether the price or volume effect dominates.For example, the increase in export volumes and decrease in import volumes are not sufficient to outweigh the fact that less is received for exports in the foreign currency and more has to be paid for imports in the domestic currency.The result is that the current account moves from balance into deficit; the increased export volumes and decreased volume of imports exactly match the decreased earnings per unit of exports and increased expenditure per unit of imports so that the current account is unchanged; the increased volume of export sales and decreased volume of imports are sufficient to outweigh the price effects so that the current balance improves following a devaluation.

The possibility that the devaluation may lead to a worsening rather than improvement in the balance of payments led to much research into empirical estimates of the elasticity of demand for exports and imports.Economists were divided up into two camps popularly known as “elasticity optimists” who believed that the sum of these two elasticity tended to exceed unity, and “elasticity pessimists” who believed that the elasticity tended to be less than unity.It was argued that a devaluation may work better for industrialized countries than for developing countries.Many developing countries are heavily dependent upon imports so that their price elasticity of demand for imports is likely to be very low.While for industrialized countries that have to face competitive export markets, the price elasticity of demand for their exports may be quite elastic.The implication of the Marshall-Lerner condition is that devaluation may be a cure for some countries’ balance of payments deficits but not for others.

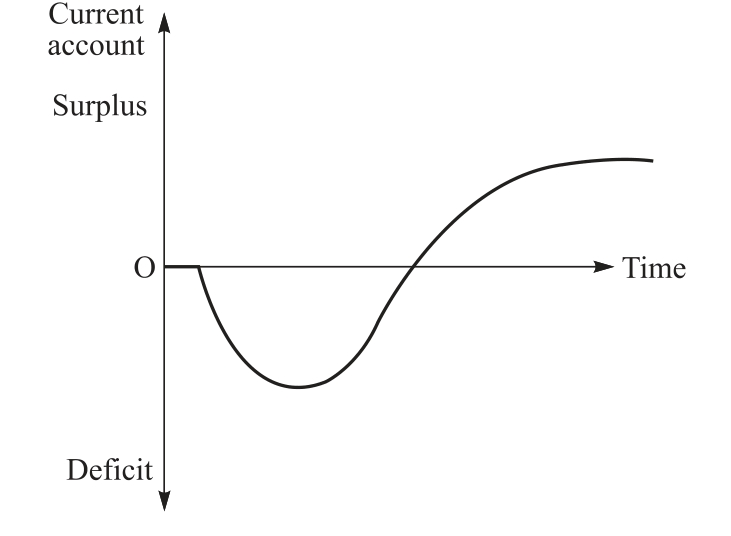

A general consensus accepted by most economists is that elasticity is lower in the short run than in the long run, in which case the Marshall-Lerner conditions may only hold in the medium to long run.This possibility leads to the phenomenon of what is popularly known as the J-curve effect, which is illustrated in Figure 2.1.The idea underlying the J-curve effect is that in the short run export volumes and import volumes do not change much, so that the price effect outweighs the volume effect leading to deterioration in the current account.However, after a time lag export volumes start to increase and import volumes start to decrease; consequently the current deficit starts to improve and eventually moves into surplus.The issue then is whether the initial deterioration in the current account is greater than the future improvement so that overall devaluation can be said to work.

Figure 2.1 The J-curve effect

There have been numerous reasons advanced to explain the slow responsiveness of export and import volumes in the short run and why the response is far greater in the longer run; three of the most important are:

A time lag in consumer response—It takes time for consumers in both the devaluing country and the rest of the world to respond to the changed competitive situation.Switching away from foreign imported goods to domestically produced goods inevitably takes some time because consumers will be worried about issues other than the price change such as the reliability and reputation of domestic produced goods as compared to the foreign imports, while foreign consumers may be reluctant to switch away from domestically produced goods towards the exports of the devaluing country.

A time lag in producer response—Even though the devaluation improves the competitive position of exports it will take time for domestic producers to expand production exportable.In addition, orders for imports are normally made well in advance and such contracts are not readily cancelled in the short run.Factories will be reluctant to cancel orders for vital inputs and raw materials.For example, the waiting list for a Boeing aeroplane can be over five years, and it is most unlikely that a British airline will cancel the order just because the pound has been devalued.Also the payments for many imports will have been hedged against exchange risk in the forward market and so will be left unaffected by the devaluation.

Imperfect competition—Building up a share of foreign markets can be a time-consuming and costly business.This being the case, foreign exporters may be very reluctant to lose their market share in the country of currency devaluation and might respond to the loss in their competitiveness by reducing their export prices.To the extent that they do this the rise in the cost of imports caused by the devaluation will be partly offset.Similarly, foreign importers may react to the threat of increased exports by reducing prices in their home markets, limiting the amount of additional exports by the country of currency devaluation.These effects rely upon some degree of imperfect competition which gives foreign firms some supernormal profit margins enabling them to reduce their prices.If foreign firms were in a highly competitive environment they would only be making normal profits and so would be unable to reduce their prices.

In addition to the above effects it is unlikely that the price of exports as measured in the domestic prices will remain fixed.Many imports are used as inputs for exporting industries, and the increased price of imports may lead to higher wage costs as workers seek compensation for higher import prices; this will to some extent lead to a rise in export prices reducing the competitive advantage of the devaluation.