Other hedging instruments

Hedging with foreign currency loans

Besides the foreign exchange risk, a company that has accounts receivable in foreign currency also has to worry about financing its claim.As we have seen, using forward contracts solves the problem of foreign exchange risk but it does not solve the financing problem.Financing in foreign currency solves both problems simultaneously.Furthermore, the technique is simple, easy to set up and accessible to medium-sized companies.

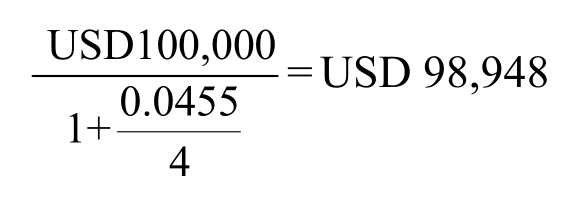

Take the example of a French wine exporter who has just signed a contract with a US importer for USD 100,000 worth of wine to be paid for in three months.A Parisian bank has offered the exporter the opportunity of borrowing dollars at the rate of Pibor plus 0.25%.the spot bid rate for dollars is 0.9000 and three-month dollar Pibor is 4%.The company’s borrowing cost is thus 4.25% per year.It will use the USD 100,000 income from the wine sale to pay off the loan, so it should borrow

At the end of three months it will owe USD 100,000, comprising USD 98,949 in principal and USD 1,051 in interest.There is no exchange risk because it can use the dollar income from its sale to the American importer to pay off the USD 100,000.Meanwhile it has USD 98,949 that it can convert into euros and use to finance its activity.

This type of operation is especially attractive to professionals when interest rates in foreign currency are low.Nevertheless, it should not be forgotten that the premium on the forward dollar offsets the interest rate advantage.Still, borrowing in foreign currency can be advantageous insofar as it reduces the number of transactions (the forward transaction is eliminated)and the Eurocurrency market is generally more competitive than domestic financial markets and spreads are lower.

For companies with a foreign exchange liability, the Eurocurrency markets can also be used to cover, as we have already mentioned.In this case, the company buys foreign currency on the spot market and then sets up a foreign currency loan to coincide with the future foreign currency payment.This type of transaction has the disadvantage of tying up the company’s money for the duration of the loan.Only companies with excess liquidity would find it advantageous and then only if the conditions in foreign currency are better than those available in the national market.

Another instrument for managing currency risk and financing problems that was popular in the 1980s is the multi-option financing facility (MOFF).A MOFF allows for the issuance of Euro-notes and short-term bank advances by competitive bidding against a variety of funding bases and currencies.If notes/advances cannot be issued at an acceptable rate, the issuer typically draws on a backstop revolving credit facility.MOFFs have the advantage of leaving companies with a wide latitude concerning the choice about when to finance and in what currency.

Swap markets

A swap is an exchange of streams of payments between two counterparties, either directly or through an intermediary.They are useful for cash management in a multi-currency environment.

1.Foreign exchange swaps

Foreign exchange swaps involves a spot buy (sale)of foreign exchange and a simultaneous offsetting forward sale (buy).They are useful when a treasurer is confronted with a temporary excess in one currency and a shortage in another.

Suppose, for example, that a treasurer of a multinational company has GBP 100,000 that he will not need for 30 days and a current shortage of marks.Rather than lending the pounds and borrowing the marks, he can make a swap with his banker.He sells the GBP 100,000 for Swiss francs at the spot rate.At the same time he makes a 30-day forward contract to sell the francs and buy the pounds back.

2.Fixed rate currency swaps

In the case of a fixed rate currency swap a company seeks to exchange a loan in one currency for a loan in another.Three stages are involved.Firstly, the principal is exchanged at the spot rate.Secondly, on each coupon date interest payments are exchanged.Finally, at the swap’s maturity the principal is re-exchanged, usually at the original exchange rate.

Hedging with insurance

Many countries have insurance organizations that provide protection against foreign exchange risk.Most of the industrialized countries have organizations of this type that are linked directly or indirectly to the government.The focus of these organizations is on commercial and political risk but many of the policies they offer also cover foreign exchange risk.

![]()

1.Purchasing power parity is based on the law of one price.It states that the exchange rate between one currency and another is in equilibrium when the domestic purchasing powers of each currency are equivalent at that rate.The empirical evidence suggests that although short-term deviations from PPP are frequent, there is a strong tendency for it to hold in the long run.

2.Covered interest parity is an application of the law of one price to financial markets.It implies that when the foreign exchange risk is covered in the forward market, then the rates of return on domestic and foreign assets with similar risk characteristics must be equal.

3.A violation of the CIP equilibrium condition triggers covered interest arbitrage.The latter, by changing the forces of supply and demand in the foreign exchange and money markets, restores the equilibrium condition.

4.The presence of bid-offer spreads reduces the profitability of covered arbitrage.

5.In an efficient market, prices reflect all available information.If information pertains to past prices only, then the market is weakly efficient.If the relevant information set contains publicly available information as well, the market is efficient in a semi-strong sense.If the information set includes insider and private information, the market is efficient in a strong sense.

6.Uncovered interest parity describes the relationship between exchange rates and interest rates.It tells us that a currency that offers a high interest rate must be expected to depreciate and vice versa.

7.The hedging instrument used is the one that produces the smallest domestic currency value of the payables and the largest domestic currency value of the receivables.